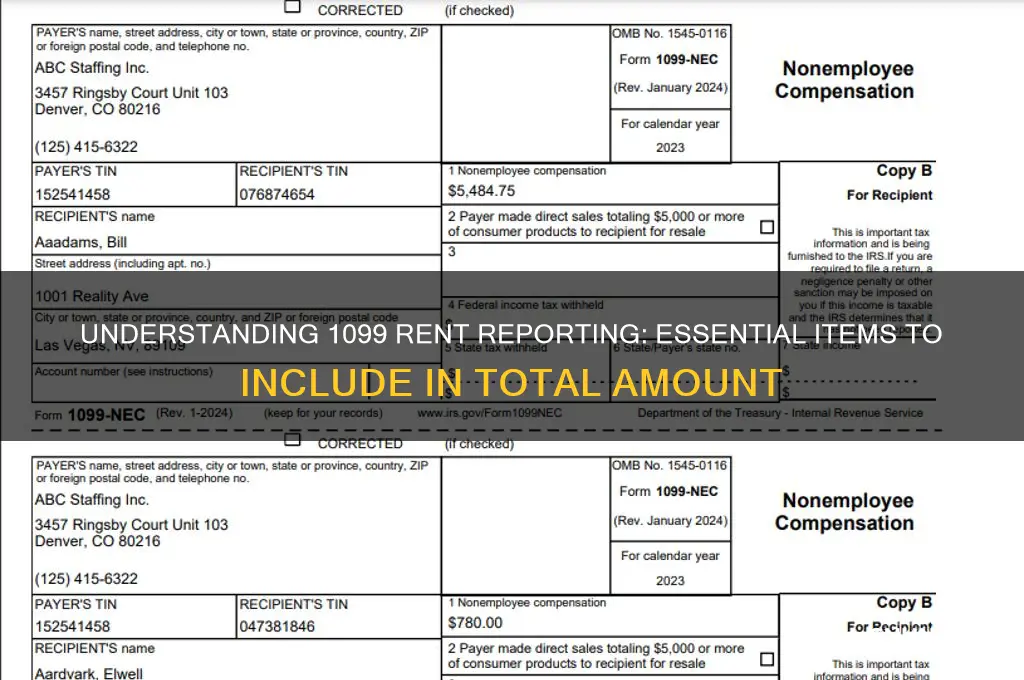

When reporting rental income on a 1099 form, it’s crucial to include the total amount of rent received from tenants during the tax year, excluding any refundable security deposits or advance rent payments for future periods. The 1099 rent amount should encompass all cash payments, property or services received in lieu of rent, and any lease cancellation fees or penalties. However, it’s important to exclude non-rent payments, such as reimbursements for utilities or maintenance, as these are not considered rental income. Properly identifying and reporting the correct rent amount ensures compliance with IRS regulations and avoids potential penalties or audits.

Explore related products

What You'll Learn

![]()

Security Deposits: Include if applied to rent, not refundable deposits

Security deposits often confuse landlords and tenants alike when it comes to 1099 reporting. The IRS is clear: only include security deposits in the 1099 rent amount if they are applied to rent during the tax year. For example, if a tenant’s $1,200 security deposit covers unpaid rent in December, that $1,200 must be reported on the 1099-NEC (not the 1099-MISC, as rent reporting has shifted). However, if the deposit is returned in full or held as a refundable security, it remains excluded from taxable rent income. This distinction hinges on whether the funds are used for rent or merely held as collateral.

Consider a scenario where a tenant vacates the property, and the landlord retains $500 of a $1,000 deposit for repairs. If the lease agreement specifies that the deposit can cover unpaid rent or damages, the $500 applied to repairs is not taxable rent. However, if the landlord applies the $500 to January’s rent (even if the tenant has already left), it becomes taxable income for that year. Documentation is critical here—ensure lease agreements clearly outline deposit usage and maintain records of all transactions to support 1099 reporting decisions.

A common mistake is treating all retained deposits as taxable income. For instance, a landlord might withhold $300 for cleaning fees and assume it’s reportable. But unless the deposit explicitly covers rent (e.g., “last month’s rent” held in advance), it’s not taxable. State laws further complicate this—some require deposits to be held in separate accounts, while others dictate specific conditions for retention. Always cross-reference state regulations with IRS guidelines to avoid over-reporting or penalties.

To navigate this effectively, follow these steps: First, review lease agreements to identify how deposits are classified (refundable vs. applied to rent). Second, track all deposit transactions throughout the year, noting when and how funds are applied. Third, consult a tax professional if deposits are used for both rent and damages, as prorating may be necessary. Finally, update 1099 forms only when deposits directly offset rent obligations, ensuring compliance without overstating income. This precision protects both landlords and tenants from tax discrepancies.

Renting Retail Space at LIRR Stations: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Late Fees: Add if charged for overdue payments

Late fees, when levied for overdue rent payments, must be included in the 1099 rent amount reported to the IRS. This is a critical detail often overlooked by landlords, yet it directly impacts tax obligations for both parties. The IRS considers late fees as additional income derived from the rental property, making them subject to the same reporting requirements as rent itself. Failure to include these fees can result in penalties or audits, underscoring the need for meticulous record-keeping and compliance.

To ensure accuracy, landlords should establish a clear policy for late fees in the lease agreement, specifying the amount, grace period, and conditions under which fees are applied. For example, a common structure is a flat fee of $50 for payments received after the 5th day of the month. Once a late fee is charged, it must be documented separately from the rent payment in accounting records. This separation simplifies the process of adding the fee to the total 1099 reportable amount at year-end.

A comparative analysis reveals that while some landlords may view late fees as a punitive measure, the IRS treats them as taxable income. This distinction highlights the dual purpose of late fees: they incentivize timely payments while contributing to the landlord’s taxable rental income. Tenants, on the other hand, should be aware that late fees increase the total amount reported on their 1099, which could affect their tax deductions or liabilities if they use the property for business purposes.

Practical implementation involves integrating late fees into the 1099 reporting process seamlessly. Landlords using property management software can automate the tracking of late fees, ensuring they are included in the annual 1099-NEC or 1099-MISC form. For manual record-keepers, a spreadsheet with columns for rent, late fees, and total payments can prevent oversight. The key is consistency—every late fee charged must be accounted for and reported to avoid discrepancies that could trigger IRS scrutiny.

In conclusion, late fees are not just a tool for enforcing payment discipline but a taxable component of rental income. Landlords must treat them with the same diligence as rent payments, ensuring they are documented, tracked, and reported accurately. By doing so, they not only comply with tax laws but also maintain transparency and trust in landlord-tenant relationships.

Renting a Billboard for a Day: A Quick Guide

You may want to see also

Explore related products

![]()

Pet Rent: Include monthly pet fees if applicable

Pet rent is a monthly fee charged to tenants who have pets in their rental units, and it should be included in the 1099 rent amount if applicable. This fee is separate from the security deposit or one-time pet fee, which are typically non-refundable and cover potential damages. Pet rent, on the otherhand, is a recurring charge that contributes to the landlord's income and should be reported as such. According to IRS guidelines, any income received from rental properties, including pet rent, must be reported on a 1099 form if the total amount exceeds $600 per year.

To accurately include pet rent in the 1099 rent amount, landlords must first establish a clear pet policy in the lease agreement. This policy should specify the monthly pet rent fee, which can vary depending on factors like the type, size, or number of pets allowed. For instance, a landlord might charge $25 per month for a single cat or $50 per month for two dogs. These fees should be consistently applied and documented to ensure compliance with tax regulations. Tenants should also be informed that pet rent is a taxable income for the landlord and will be reported accordingly.

One common mistake landlords make is failing to differentiate between pet rent and pet deposits. While pet deposits are typically held to cover potential damages and may be refundable, pet rent is a recurring charge for the privilege of having a pet in the unit. For example, if a tenant pays a $300 pet deposit and $30 monthly pet rent, only the $30 monthly fee should be included in the 1099 rent amount. Landlords should maintain separate records for these transactions to avoid confusion and ensure accurate reporting.

From a tenant’s perspective, understanding that pet rent is part of the overall rental cost is crucial. Tenants should budget accordingly and be aware that this fee is non-negotiable in most cases. For landlords, clearly communicating the purpose of pet rent can help justify the charge and reduce disputes. For instance, explaining that pet rent helps cover additional wear and tear, maintenance, or administrative costs associated with pet-friendly units can provide transparency and foster a positive landlord-tenant relationship.

In conclusion, including monthly pet fees in the 1099 rent amount is a straightforward yet often overlooked aspect of rental income reporting. By establishing clear policies, maintaining accurate records, and educating both landlords and tenants, this process can be streamlined and compliant with tax laws. Whether you’re a landlord or a tenant, recognizing the role of pet rent in rental agreements ensures financial transparency and avoids potential legal pitfalls.

Understanding Rent-A-Center's Interest Rates: What You Need to Know

You may want to see also

Explore related products

![]()

Utilities: Add if landlord pays and charges tenant

Landlords often cover utility expenses as part of their property management, but when these costs are passed on to tenants, it raises questions about tax reporting. The IRS considers rent to include any payments received for the use or occupancy of property, and this broad definition can encompass more than just the base rent. If a landlord pays for utilities such as electricity, water, or gas and then charges the tenant for these services, the amounts collected should be included in the total rent reported on a 1099-MISC or 1099-NEC form. This ensures compliance with tax regulations and provides a clear financial picture for both parties.

Consider a scenario where a landlord pays a monthly electricity bill of $150 for a rental unit and charges the tenant this exact amount. While the landlord is merely recouping the expense, the IRS views this transaction as part of the rental income. Failure to include such amounts in the 1099 rent figure could lead to underreporting, potentially triggering audits or penalties. To avoid these issues, landlords should meticulously track utility payments and reimbursements, ensuring they are accurately reflected in tax documents.

From a practical standpoint, landlords can simplify this process by clearly outlining utility charges in the lease agreement. For instance, specifying that tenants will be billed for utilities based on actual usage or a flat monthly fee provides transparency. When tax season arrives, landlords can sum these charges alongside the base rent to determine the total amount to report on the 1099 form. This approach not only adheres to IRS guidelines but also fosters trust with tenants by maintaining clear financial records.

One common misconception is that utility reimbursements are separate from rent and thus exempt from 1099 reporting. However, the IRS treats these payments as part of the rental income, regardless of how they are labeled. Landlords who manage multiple properties or handle varying utility arrangements should use accounting software or spreadsheets to track these expenses systematically. By doing so, they can ensure that every dollar collected for utilities is accounted for in their tax filings, minimizing the risk of errors.

In conclusion, including utility charges in the 1099 rent amount is not just a best practice—it’s a requirement. Landlords who pay for utilities and recoup these costs from tenants must treat these reimbursements as rental income for tax purposes. By maintaining detailed records and understanding IRS guidelines, landlords can navigate this aspect of property management with confidence, ensuring both compliance and financial clarity.

How to Verify VRBO Rental Payments: A Step-by-Step Guide for Hosts

You may want to see also

Explore related products

![]()

Prepaid Rent: Include advance payments for future rent periods

Advance payments for future rent periods, often referred to as prepaid rent, must be included in the 1099 rent amount to ensure compliance with IRS regulations. These payments represent income received in the current tax year, even if they cover rental periods extending into the future. For example, if a tenant pays $12,000 in December 2023 for rent covering January to June 2024, the entire $12,000 must be reported on the landlord’s 1099-NEC or 1099-MISC for the 2023 tax year. Failure to include prepaid rent can result in underreporting income, triggering audits or penalties.

The rationale behind this rule is straightforward: the IRS considers income taxable when it is received, not when it is earned. This principle applies universally, whether the prepaid rent covers one month or multiple years. Landlords should carefully review lease agreements to identify any advance payments and ensure they are accurately reflected in their tax filings. For instance, if a commercial tenant prepays $50,000 for a five-year lease, the full amount is reportable in the year of receipt, regardless of the lease term.

One common mistake landlords make is prorating prepaid rent across future years. This approach is incorrect and can lead to discrepancies in tax reporting. Instead, landlords should report the full amount in the year received and adjust their accounting records to reflect the deferred income. For example, if $6,000 is prepaid for 2024 rent in 2023, the landlord reports $6,000 in 2023 but recognizes the income over the rental period in their books.

To streamline compliance, landlords should maintain detailed records of all rental transactions, including prepaid amounts, payment dates, and corresponding lease periods. Using accounting software with 1099 reporting features can automate this process, reducing the risk of errors. Additionally, consulting a tax professional can provide clarity on complex scenarios, such as partial prepayments or lease renewals with advanced rent.

In conclusion, prepaid rent is a critical component of the 1099 rent amount, requiring careful attention to timing and reporting. By including advance payments in the current tax year and maintaining accurate records, landlords can avoid legal pitfalls and ensure financial transparency. This proactive approach not only satisfies IRS requirements but also fosters trust with tenants and stakeholders.

U-Haul Rental Deposits: What You Need to Know Before Renting

You may want to see also

Frequently asked questions

The 1099 rent amount should include all rent payments received from the tenant during the tax year, including any advance rent payments or prepaid rent.

No, security deposits should not be included in the 1099 rent amount unless they are applied to rent or forfeited by the tenant. In that case, the amount applied to rent should be included.

Yes, late fees and other charges related to the rental of the property, such as pet fees or utility reimbursements, should be included in the 1099 rent amount.

No, rent payments received for prior years should not be included in the current year's 1099 rent amount. Only rent payments received during the current tax year should be reported.