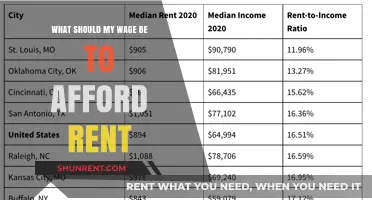

Determining the appropriate rent-to-income ratio is crucial for financial stability and long-term planning. A widely accepted guideline is that rent should not exceed 30% of your gross monthly income, as this allows for sufficient funds to cover other essential expenses, savings, and discretionary spending. Exceeding this threshold can strain your budget, increase the risk of financial stress, and limit your ability to save for emergencies or future goals. However, this rule may vary depending on individual circumstances, such as location, lifestyle, and personal financial priorities. Understanding this balance ensures that housing remains affordable while maintaining overall financial health.

| Characteristics | Values |

|---|---|

| Recommended Rent-to-Income Ratio | 30% or less |

| Source | U.S. Department of Housing and Urban Development (HUD), financial advisors |

| Rationale | Ensures affordability and prevents financial strain |

| Average Rent-to-Income Ratio in the U.S. (2023) | ~32-35% (varies by city and income level) |

| High-Cost Urban Areas (e.g., NYC, SF) | Often exceeds 40-50% due to housing market pressures |

| Low-Income Households | May spend 50% or more of income on rent |

| Impact of Exceeding 30% | Increased risk of financial instability, reduced savings, and difficulty covering other expenses |

| Alternative Metrics | 40x rent rule (monthly rent ≤ 1/40th of annual income) |

| Factors Influencing Ratio | Local cost of living, income level, household size, and personal financial goals |

| Adjustments for High Rent Areas | Consider roommates, smaller housing, or government assistance programs |

| Long-Term Financial Advice | Aim to reduce rent-to-income ratio over time through income growth or housing adjustments |

Explore related products

What You'll Learn

![]()

50/30/20 Rule Basics

Rent should not exceed 30% of your gross income, a principle rooted in the 50/30/20 budgeting framework. This rule divides your after-tax income into three categories: 50% for needs, 30% for wants, and 20% for savings and debt repayment. Housing, as a fundamental need, falls into the first category, but its allocation is not arbitrary. Exceeding the 30% threshold can strain your ability to cover other essentials or save for the future. For instance, if your monthly income is $4,000, your rent should ideally stay below $1,200. This guideline ensures financial stability and prevents the trap of being "house poor."

The 50/30/20 rule is not one-size-fits-all but a starting point for customization. High-cost-of-living areas may require adjustments, but the core principle remains: prioritize balance. If rent consumes 40% of your income, you’ll likely need to reduce spending in other areas, such as dining out or entertainment, to maintain the 50% cap on needs. Alternatively, consider increasing your income through side gigs or negotiating a raise. The rule’s flexibility allows for adaptation while keeping you accountable to its underlying philosophy: live within your means, save consistently, and avoid unnecessary debt.

Critics argue that the 50/30/20 rule may be unrealistic for low-income earners or those in expensive cities. For example, in San Francisco, where median rents surpass $3,000, adhering to the 30% rule would require an income of at least $10,000 monthly—far above the national average. In such cases, the rule may need to be recalibrated, perhaps allowing 40% for needs while reducing discretionary spending or savings temporarily. The key is to use the framework as a tool, not a rigid mandate, and to reassess periodically as your financial situation evolves.

Implementing the 50/30/20 rule begins with tracking your income and expenses. Start by calculating your monthly after-tax income, then categorize your spending over the past three months. If your rent exceeds 30%, explore options like finding a roommate, moving to a more affordable area, or renegotiating your lease. Simultaneously, scrutinize your "wants" category for cuts—perhaps reducing subscription services or cooking at home more often. Finally, automate your savings to ensure the 20% allocation is non-negotiable. Small adjustments today can lead to significant financial freedom tomorrow.

The beauty of the 50/30/20 rule lies in its simplicity and clarity. It transforms abstract financial goals into actionable percentages, making it easier to visualize and achieve balance. By capping rent at 30% of your income, you create a buffer for unexpected expenses and long-term goals like retirement or homeownership. While perfection isn’t the goal, consistency is. Over time, this approach fosters financial resilience, ensuring that your housing costs support, rather than hinder, your overall well-being.

Understanding Gross Rent in Commercial Real Estate: Definition and Implications

You may want to see also

Explore related products

![]()

Affordable Rent Thresholds

A common rule of thumb suggests that rent should not exceed 30% of your gross monthly income. This guideline, often referred to as the "30% rule," has been widely adopted by financial advisors and housing experts as a benchmark for affordability. For instance, if your monthly income is $4,000, your rent should ideally be $1,200 or less. However, this rule is not one-size-fits-all. Factors such as location, household size, and personal financial goals can significantly influence what constitutes an affordable rent threshold for you.

To determine your personalized affordable rent threshold, start by calculating your total monthly income after taxes. Next, list all essential expenses, including utilities, groceries, transportation, and savings. Subtract these from your income to find your discretionary spending. Your rent should fit comfortably within the remaining amount, ensuring you have enough for emergencies and leisure. For example, if your monthly take-home pay is $3,500 and essential expenses total $1,800, your rent should not exceed $1,050 to stay within the 30% guideline while maintaining financial stability.

Critics argue that the 30% rule is outdated, particularly in high-cost urban areas like New York or San Francisco, where housing consumes a larger portion of income. In such cases, a more realistic threshold might be 40–50% of income, but this requires careful budgeting. For instance, if you earn $5,000 monthly and live in an expensive city, a $2,000 rent (40%) might be feasible if you minimize other expenses, such as dining out or subscriptions. However, this approach leaves less room for savings or unexpected costs, making it riskier.

For low-income households or those with fluctuating incomes, affordable rent thresholds may need to be even lower. A 25% rule could be more appropriate to ensure financial resilience. For example, if your monthly income is $2,500, limiting rent to $625 allows for greater flexibility in managing other expenses. Additionally, consider government assistance programs or shared housing arrangements to further reduce housing costs. The key is to align your rent with your overall financial health, not just a generic percentage.

Ultimately, the affordable rent threshold is a dynamic concept that requires regular reassessment. Life changes—such as a new job, family expansion, or economic shifts—may necessitate adjusting your housing budget. Use online calculators or consult a financial planner to refine your threshold periodically. By staying proactive and realistic, you can ensure that your rent remains a manageable part of your income, fostering long-term financial security.

Is a Rent Acceleration Clause Enforceable in Colorado? Legal Insights

You may want to see also

Explore related products

![]()

Income-to-Rent Ratios

A common rule of thumb suggests that rent should not exceed 30% of your gross monthly income. This guideline, often referred to as the 30% rule, has been widely adopted as a benchmark for affordable housing. However, this one-size-fits-all approach may not account for individual circumstances, regional variations, and the evolving economic landscape. For instance, in high-cost urban areas like San Francisco or New York, renters often spend closer to 50% of their income on housing, while in more affordable regions, the percentage might drop to 20%. Understanding your personal income-to-rent ratio requires a more nuanced analysis than simply adhering to a blanket recommendation.

To calculate your income-to-rent ratio, divide your monthly rent by your gross monthly income and multiply by 100 to get a percentage. For example, if your monthly rent is $1,200 and your gross income is $4,000, your ratio is 30% ($1,200 / $4,000 * 100). While this calculation is straightforward, it’s crucial to consider your overall financial health. If you have significant debt, high living expenses, or savings goals, a 30% ratio might still strain your budget. Conversely, if you have minimal financial obligations, a higher ratio could be manageable. The key is to align your housing costs with your broader financial priorities.

For young professionals or those in entry-level positions, a lower income-to-rent ratio is often more sustainable. Aiming for 25% or less can provide a buffer for unexpected expenses and allow for savings or investments. On the other hand, higher earners might comfortably allocate up to 40% of their income to rent, especially if they have fewer financial commitments. Age and life stage also play a role: a single person in their 20s may prioritize location and lifestyle, while a family might prioritize space and stability, even if it means a higher rent burden.

When evaluating your income-to-rent ratio, consider regional cost-of-living differences. In cities with skyrocketing rents, even a 30% ratio may be unattainable for many. In such cases, strategies like finding roommates, choosing smaller spaces, or living farther from city centers can help balance affordability and lifestyle. Conversely, in areas with lower housing costs, allocating less than 30% to rent could free up funds for other financial goals, such as retirement savings or paying off student loans.

Ultimately, the ideal income-to-rent ratio is not a fixed number but a dynamic figure that reflects your unique financial situation and goals. While the 30% rule serves as a useful starting point, it’s essential to assess your income, expenses, and priorities holistically. By doing so, you can make informed decisions about how much to spend on rent, ensuring that your housing costs support, rather than hinder, your long-term financial well-being.

Unlock Federal Rent Checks: Join the Distribution List Today

You may want to see also

Explore related products

![]()

Regional Cost Variations

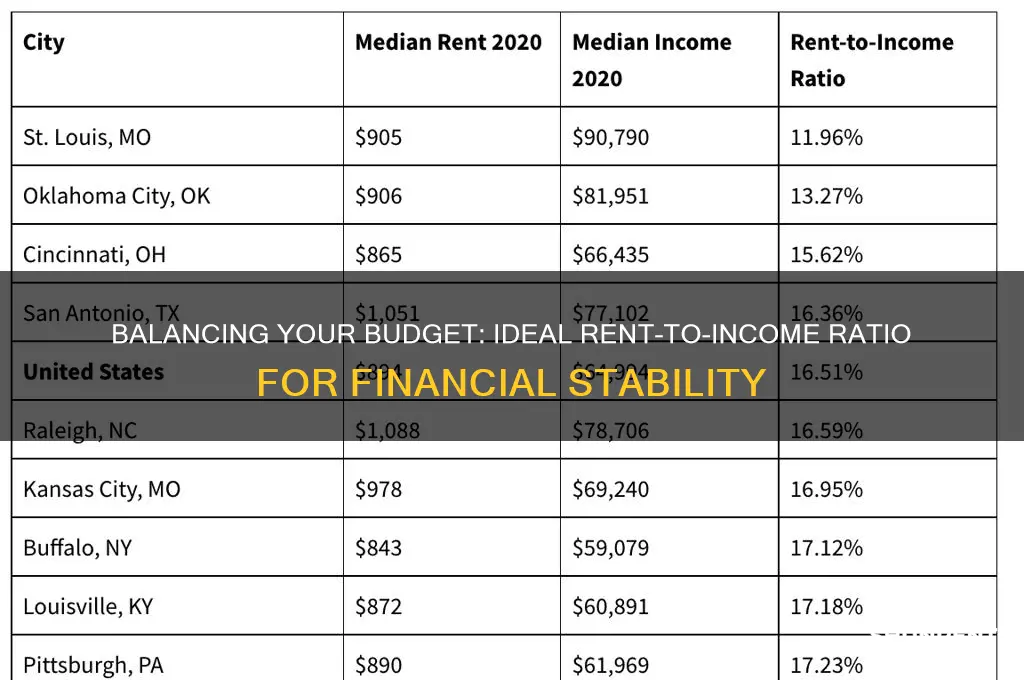

Rent-to-income ratios aren’t one-size-fits-all. A 30% threshold, often cited as ideal, crumbles under regional cost variations. In San Francisco, where median rent exceeds $3,000, even dual-income households earning $120,000 annually may struggle to meet this benchmark. Conversely, in Tulsa, Oklahoma, where median rent hovers around $850, the same ratio allows for significantly more financial flexibility. This disparity highlights the need to contextualize rent affordability by location, not universal guidelines.

Consider the Midwest versus the Northeast. In Indianapolis, a $50,000 salary comfortably covers a $1,000 monthly rent, leaving room for savings and discretionary spending. In Boston, that same income would barely cover a studio apartment, forcing renters to allocate closer to 50% of their earnings to housing. Such regional extremes demand localized budgeting strategies. For instance, in high-cost cities, renters might prioritize shared housing or negotiate lease terms, while in affordable areas, they could invest surplus income in retirement accounts or emergency funds.

Geographic cost differences also skew perceptions of "affordable" living. A New Yorker might balk at spending 40% of their income on rent, while a resident of Des Moines, Iowa, would find that percentage absurdly high. This relativity underscores the importance of benchmarking against local averages, not national ones. Tools like the U.S. Department of Housing and Urban Development’s Fair Market Rents can provide region-specific data, helping renters gauge whether they’re overpaying or securing a bargain.

Finally, regional variations intersect with lifestyle choices. In expensive coastal cities, renters often trade space for location, accepting smaller apartments to live near work or cultural hubs. In contrast, those in low-cost regions may prioritize square footage or amenities, knowing their income stretches further. Understanding these trade-offs allows renters to align their housing decisions with both financial constraints and personal priorities, ensuring affordability doesn’t come at the expense of quality of life.

Do People Still Rent Bell System Phones Today?

You may want to see also

Explore related products

![]()

Budgeting for Rent Expenses

A common rule of thumb suggests that rent should not exceed 30% of your gross monthly income. This guideline, often referred to as the 30% rule, has been widely adopted as a benchmark for affordable housing. However, this one-size-fits-all approach may not account for individual circumstances, such as high-cost urban living or fluctuating income levels. For instance, in cities like New York or San Francisco, where housing costs are significantly higher, adhering strictly to the 30% rule might be impractical for many residents. Therefore, while this rule provides a starting point, it’s essential to tailor it to your specific financial situation.

To effectively budget for rent, begin by calculating your total monthly income after taxes. Subtract all fixed expenses, such as utilities, insurance, and debt payments, to determine your disposable income. From this amount, allocate no more than 30–40% for rent, depending on your financial flexibility. For example, if your monthly take-home pay is $4,000, a rent of $1,200 (30%) would be ideal, leaving you with $2,800 for other expenses and savings. However, if you live in an expensive area, you might need to adjust this percentage upward, ensuring you still have enough for essentials and savings.

Another practical strategy is to prioritize savings alongside rent. Financial experts recommend saving at least 20% of your income for emergencies and long-term goals. If rent consumes a larger portion of your budget, consider reducing discretionary spending, such as dining out or entertainment, to maintain a balanced financial plan. For instance, cutting back on non-essential expenses by $200 monthly can offset a slightly higher rent payment while keeping your overall budget on track.

Comparing rent-to-income ratios across different income brackets highlights the need for flexibility. Lower-income households often spend a higher percentage of their income on rent, sometimes exceeding 50%, which can lead to financial strain. In contrast, higher-income earners may comfortably allocate less than 20% to housing. This disparity underscores the importance of adjusting budgeting strategies based on income level. For lower-income individuals, seeking subsidized housing or roommates can help align rent expenses with income more realistically.

Ultimately, budgeting for rent requires a personalized approach that considers your income, location, and financial goals. While the 30% rule is a useful guideline, it’s not absolute. Regularly review your budget to ensure rent remains manageable, and don’t hesitate to make adjustments if circumstances change. By striking a balance between housing costs and other financial priorities, you can achieve stability and work toward long-term financial health.

Mastering the SSA Rent Form: A Step-by-Step Guide for SSI Applicants

You may want to see also

Frequently asked questions

A common rule of thumb is to spend no more than 30% of your gross monthly income on rent. This helps ensure you have enough left for other expenses and savings.

While the 30% rule is a guideline, it may be necessary to exceed it in high-cost areas. However, aim to keep rent as close to 30% as possible to avoid financial strain.

Multiply your gross monthly income by 0.3 (30%). The result is the maximum rent you should consider. For example, if you earn $4,000/month, aim for rent under $1,200.

Yes, factor in utilities, parking, and other housing-related expenses when determining affordability to get a more accurate picture of your total housing costs.

Consider finding a more affordable place, increasing your income, or reducing other expenses to balance your budget and avoid financial stress.