When considering the type of account that rent would fall under for a business, it is important to understand that rent is typically classified as an operating expense. In accounting, rent is usually recorded as a debit to the Rent Expense account, which is a part of the income statement, and a credit to the Accounts Payable or Cash account, depending on whether the rent is paid in advance or at the time of payment. This classification ensures that the business accurately reflects its financial obligations and expenses related to occupying a property, whether it be an office, retail space, or warehouse, and helps in maintaining a clear and organized financial record for tax and reporting purposes.

| Characteristics | Values |

|---|---|

| Account Type | Expense Account |

| Category | Operating Expense |

| Nature | Non-Current (if prepaid) / Current (if paid monthly) |

| Financial Statement Impact | Reduces Net Income on Income Statement |

| Tax Treatment | Tax-Deductible (reduces taxable income) |

| Recording Method | Debit Rent Expense, Credit Cash/Accounts Payable |

| Common Sub-Accounts | Rent - Office, Rent - Equipment, Rent - Retail Space |

| Accrual Basis | Recorded when incurred, not when paid (if using accrual accounting) |

| Cash Basis | Recorded when payment is made |

| Prepaid Rent | Asset account (Prepaid Rent) until expense is recognized |

| Relevance | Essential for businesses leasing property or equipment |

| Audit Trail | Requires lease agreements and payment receipts for verification |

Explore related products

$18.1 $35

What You'll Learn

- Expense Account Classification: Rent is typically classified as an operating expense in a business's income statement

- Prepaid Rent Handling: Prepaid rent is recorded as an asset until the rental period is utilized

- Lease Accounting Standards: Rent under operating leases is expensed directly, while capital leases are capitalized

- Tax Deductibility: Rent payments are generally tax-deductible as a business expense, reducing taxable income

- Cash vs. Accrual Basis: Rent is expensed when paid (cash basis) or when incurred (accrual basis)

![]()

Expense Account Classification: Rent is typically classified as an operating expense in a business's income statement

Rent, a ubiquitous cost for most businesses, is not merely a line item on a ledger; it is a critical component of a company's financial health. In accounting, rent is typically classified as an operating expense, a designation that carries significant implications for financial reporting and analysis. This classification is rooted in the nature of rent as a necessary, ongoing cost directly tied to the day-to-day operations of a business. For instance, a retail store’s lease payment for its storefront is essential for maintaining its physical presence and generating revenue, making it an operating expense rather than a capital expenditure.

Understanding this classification is crucial for accurate financial statement preparation. Operating expenses are reported on the income statement and directly impact a company’s operating income, a key metric for assessing profitability. Rent, alongside other operating expenses like utilities and salaries, provides a clear picture of the costs incurred to run the business. For example, a small business owner analyzing their income statement can quickly identify whether rent is consuming an unsustainable portion of their revenue, prompting strategic decisions such as renegotiating lease terms or relocating.

However, not all rent payments are treated equally. While most rent expenses fall under operating expenses, certain scenarios may warrant different classifications. For instance, if a business leases equipment or vehicles, these costs might be categorized as operating leases or, in some cases, capitalized under specific accounting standards like ASC 842. This distinction highlights the importance of understanding the nuances of lease accounting, particularly for businesses with diverse rental agreements. Misclassification can distort financial ratios and mislead stakeholders about the company’s operational efficiency.

From a practical standpoint, proper classification of rent as an operating expense simplifies tax reporting and compliance. Operating expenses are generally tax-deductible in the year they are incurred, reducing taxable income. For example, a tech startup paying $5,000 monthly rent for office space can deduct this amount from its taxable income, easing its tax burden. However, businesses must maintain detailed records and ensure that rent payments are solely for operational purposes to avoid scrutiny from tax authorities.

In conclusion, classifying rent as an operating expense is more than an accounting formality; it is a reflection of its role in sustaining business operations. This classification enables stakeholders to evaluate a company’s operational efficiency, make informed decisions, and ensure compliance with financial regulations. By mastering this concept, business owners and accountants can maintain accurate financial records and strategically manage one of the most significant costs in their operations.

Renting Cleveland City Parks: A Step-by-Step Guide for Events

You may want to see also

Explore related products

![]()

Prepaid Rent Handling: Prepaid rent is recorded as an asset until the rental period is utilized

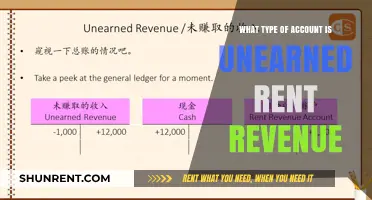

Prepaid rent is a unique accounting entry that requires careful handling to ensure financial accuracy. When a business pays rent in advance, it’s not immediately expensed. Instead, it’s recorded as a current asset on the balance sheet under the account "Prepaid Rent" or "Prepaid Expenses." This classification reflects the future economic benefit the business will receive over the rental period. For example, if a company pays $12,000 for a year’s rent in January, only $1,000 is expensed monthly as rent expense, while the remaining balance is gradually reduced. This method aligns with the matching principle, ensuring expenses are recognized in the period they are incurred.

The process of handling prepaid rent involves two key steps. First, when the payment is made, debit the prepaid rent account (asset) and credit cash (asset). This records the transaction without immediately affecting the income statement. Second, as each rental period passes, adjust the entry by debiting rent expense (expense) and crediting prepaid rent (asset). For instance, if a business prepays $6,000 for six months of rent, it would debit prepaid rent for $6,000 and credit cash for $6,000. Each month, $1,000 is then moved from prepaid rent to rent expense. This systematic approach ensures the financial statements accurately reflect the business’s financial position and performance.

A common mistake in prepaid rent handling is treating the entire payment as an immediate expense, which distorts both the income statement and balance sheet. For example, expensing $12,000 of prepaid rent in January would overstate that month’s expenses and understate assets. Conversely, failing to recognize the expense monthly would overstate assets and understate expenses. To avoid these errors, businesses should establish a clear accounting policy for prepaid rent, supported by regular reviews and reconciliations. Software tools like QuickBooks or Excel templates can automate these adjustments, reducing the risk of manual errors.

From a comparative perspective, prepaid rent differs from other prepaid expenses like insurance or utilities in its direct link to a specific asset—the rented space. While all prepaid expenses are initially recorded as assets, rent often represents a larger financial commitment and longer time horizon. For instance, a business might prepay $500 for three months of internet service, but $12,000 for a year’s rent. This distinction highlights the importance of tailored accounting practices for prepaid rent, ensuring it’s managed separately from other prepaid items. By doing so, businesses maintain clarity and precision in their financial reporting.

In conclusion, prepaid rent handling is a critical aspect of business accounting that demands precision and consistency. By recording prepaid rent as an asset and systematically expensing it over the rental period, businesses adhere to accounting principles while maintaining accurate financial records. Practical tips include using accounting software for automated adjustments, conducting monthly reconciliations, and training staff to recognize the unique treatment of prepaid rent. Mastering this process not only ensures compliance but also provides a clear picture of a business’s financial health and resource allocation.

Waterfront's Premium Office Space for Rent

You may want to see also

Explore related products

![]()

Lease Accounting Standards: Rent under operating leases is expensed directly, while capital leases are capitalized

Rent, a ubiquitous expense for businesses, is not a one-size-fits-all entry in the accounting ledger. The treatment of rent hinges on the nature of the lease agreement, with operating leases and capital leases dictating distinct accounting paths. Under the lease accounting standards, primarily governed by ASC 842 in the U.S. and IFRS 16 internationally, rent under operating leases is expensed directly in the income statement as incurred. This means the entire rent payment is recognized as an expense in the period it is paid, reflecting the short-term, non-ownership nature of the lease. For instance, a retail store renting a storefront under an operating lease would record the monthly rent as an operating expense, reducing net income proportionally each month.

In contrast, capital leases, now often referred to as finance leases under updated standards, are treated as if the leased asset were owned by the lessee. Here, rent is not expensed directly. Instead, the lease payments are bifurcated into interest expense and a reduction of the lease liability, while the leased asset is capitalized on the balance sheet. This approach aligns with the economic reality of the lease, where the lessee effectively gains control and benefits akin to ownership. For example, a manufacturing company leasing machinery under a finance lease would record the present value of future lease payments as an asset and a liability, depreciating the asset over its useful life while expensing the interest portion of the payments.

The distinction between these treatments has significant implications for financial statements. Operating leases preserve cash flow neutrality in the short term but keep the balance sheet lighter, as no asset or liability is recorded. Capital leases, however, increase both assets and liabilities, providing a more comprehensive view of the company’s long-term obligations and resource utilization. For investors and analysts, understanding this classification is crucial for assessing a company’s financial health, leverage, and operational efficiency.

Practical application of these standards requires careful lease analysis. Key criteria include the lease term relative to the asset’s useful life, the present value of lease payments compared to the asset’s fair value, and options for purchase or renewal. Businesses must scrutinize lease agreements to determine the appropriate classification, ensuring compliance with accounting standards and accurate financial reporting. For instance, a lease with a term covering 75% of the asset’s useful life or payments totaling 90% of its fair value would typically qualify as a finance lease, necessitating capitalization.

In summary, the accounting treatment of rent is not merely a technicality but a reflection of the economic substance of the lease. Operating leases simplify expense recognition, while capital leases provide a more holistic financial picture. By mastering these distinctions, businesses can ensure transparency, compliance, and informed decision-making, turning a routine expense into a strategic accounting tool.

Rent Loan Approval Timeline: How Long Do Banks Typically Take?

You may want to see also

Explore related products

![]()

Tax Deductibility: Rent payments are generally tax-deductible as a business expense, reducing taxable income

Rent payments are a significant expense for many businesses, but they also offer a valuable tax advantage. When a business leases property for operations, these payments are typically classified as a business expense, making them tax-deductible. This deduction directly reduces taxable income, lowering the overall tax liability. For example, if a small business pays $2,000 monthly in rent and falls into the 25% tax bracket, deducting this expense saves $600 annually in taxes. This financial benefit underscores the importance of properly categorizing rent payments in accounting records.

To maximize this deduction, businesses must ensure rent payments are ordinary and necessary for operations. The IRS requires that the expense be both common in the industry and helpful for generating income. For instance, renting office space for employees or a retail store for customers qualifies, but leasing a personal residence for business use may face scrutiny. Maintaining clear documentation, such as lease agreements and payment receipts, is essential to substantiate the deduction during audits.

A common pitfall is misclassifying rent payments, particularly for home-based businesses. If a business owner uses part of their home exclusively and regularly for business, they may deduct a portion of rent or mortgage interest using the home office deduction. However, this requires precise calculations based on the percentage of space used for business. For example, if 20% of a home is dedicated to business, only that portion of rent is deductible. Missteps here can lead to disallowed deductions or penalties.

Comparatively, rent deductions differ from other expenses like depreciation. While rent is a current expense deducted in the year paid, depreciation spreads the cost of owned property over its useful life. Businesses leasing equipment or vehicles may also deduct these payments, but the rules vary. For instance, vehicle lease payments are deductible if used primarily for business, but personal use reduces the allowable amount. Understanding these distinctions ensures accurate tax reporting and maximizes savings.

In practice, businesses should consult tax professionals to navigate complexities, especially when operating in multiple jurisdictions with varying tax laws. For instance, state and local taxes may treat rent deductions differently than federal guidelines. Additionally, businesses should review their lease agreements for escalation clauses or additional fees, as these may also be deductible if directly tied to business use. By strategically managing rent payments and leveraging tax deductions, businesses can improve cash flow and reinvest savings into growth initiatives.

Affordable Brentwood CA Rentals: Tips to Find Your Perfect Cheap Apartment

You may want to see also

Explore related products

![]()

Cash vs. Accrual Basis: Rent is expensed when paid (cash basis) or when incurred (accrual basis)

Rent, a significant expense for many businesses, is treated differently under cash and accrual accounting methods. This distinction directly impacts financial reporting and tax obligations.

Understanding the difference is crucial for accurate record-keeping and informed decision-making.

Cash Basis: Simplicity with Limitations

Imagine a small retail store paying monthly rent of $2,000. Under the cash basis, this expense is only recognized when the payment is actually made. If the store pays rent on the 1st of each month, the $2,000 expense appears in that month's financial statements. This method is straightforward, mirroring the business's cash flow. However, it can distort the true financial picture. If the store pays rent for December in January, December's expenses appear artificially low, while January's appear inflated. This lack of matching expenses with the period they relate to can make it difficult to assess the business's true profitability in a given period.

This method is often used by smaller businesses due to its simplicity, but it may not provide a complete financial snapshot.

Accrual Basis: Matching Expenses to Revenue

In contrast, the accrual basis focuses on when the expense is incurred, not when it's paid. Using our retail store example, the $2,000 rent expense for December would be recorded in December, even if the payment is made in January. This method aligns expenses with the period they contribute to generating revenue, providing a more accurate representation of the business's financial performance. For instance, if the store generates $10,000 in sales in December, recognizing the rent expense in the same month gives a clearer picture of December's profitability.

Choosing the Right Method: Considerations

The choice between cash and accrual basis depends on several factors. Small businesses with straightforward transactions and a desire for simplicity may find the cash basis sufficient. However, businesses seeking a more accurate financial picture, especially those with significant accruals or aiming to attract investors, often opt for the accrual basis. Tax regulations also play a role, as some jurisdictions require accrual accounting for businesses above a certain size or revenue threshold.

Practical Tip:

Businesses transitioning from cash to accrual basis accounting should carefully review their rent agreements and ensure proper documentation of rent expenses incurred but not yet paid. This ensures a smooth transition and accurate financial reporting under the new method.

Rent-to-Own Explained: Benefits, Risks, and Key Considerations

You may want to see also

Frequently asked questions

Rent is typically categorized as an expense account for a business, specifically under operating expenses or selling, general, and administrative expenses (SG&A).

Rent is considered an expense, not a liability. However, any prepaid rent or rent due but not yet paid may be recorded as a current liability until it is expensed.

Rent falls under the expense category in a chart of accounts, often listed as "Rent Expense" or "Occupancy Costs."

No, rent is not classified as an asset. It is an expense that reduces the business's net income, as it represents a cost of using a property or space.

When rent is paid in advance, it is initially recorded as a prepaid expense (asset). As the rental period progresses, the prepaid amount is gradually expensed to the rent expense account.