The classification of rent deposits as current or long-term assets depends on the specific accounting framework and the lease agreement's terms. Under generally accepted accounting principles (GAAP) and International Financial Reporting Standards (IFRS), rent deposits are typically treated as prepaid expenses, which are considered current assets if they are expected to be utilized within one year or the operating cycle, whichever is longer. However, if the lease agreement spans multiple years and the deposit is not refundable or will be applied to future rent payments beyond the current fiscal year, it may be classified as a long-term asset. This distinction is crucial for financial reporting and analysis, as it impacts the balance sheet presentation and the assessment of a company's liquidity and long-term financial health.

| Characteristics | Values |

|---|---|

| Classification | Rent deposits are typically classified as current liabilities if they are expected to be refunded within one year or the operating cycle, whichever is longer. If held for longer, they may be classified as long-term liabilities. |

| Accounting Treatment | Recorded as a liability on the balance sheet until refunded or applied to rent. |

| Refundability | Usually refundable at the end of the lease term, provided there are no damages or unpaid rent. |

| Time Frame | Current if refundable within 12 months; long-term if beyond 12 months. |

| Purpose | Security for the landlord against potential damages or unpaid rent. |

| Reporting Standards | Under GAAP and IFRS, classified based on the expected refund period. |

| Impact on Financial Statements | Increases current liabilities if short-term; increases long-term liabilities if long-term. |

| Common Practice | Most rent deposits are treated as current liabilities due to their short-term nature. |

Explore related products

What You'll Learn

![]()

Deposit Classification Criteria

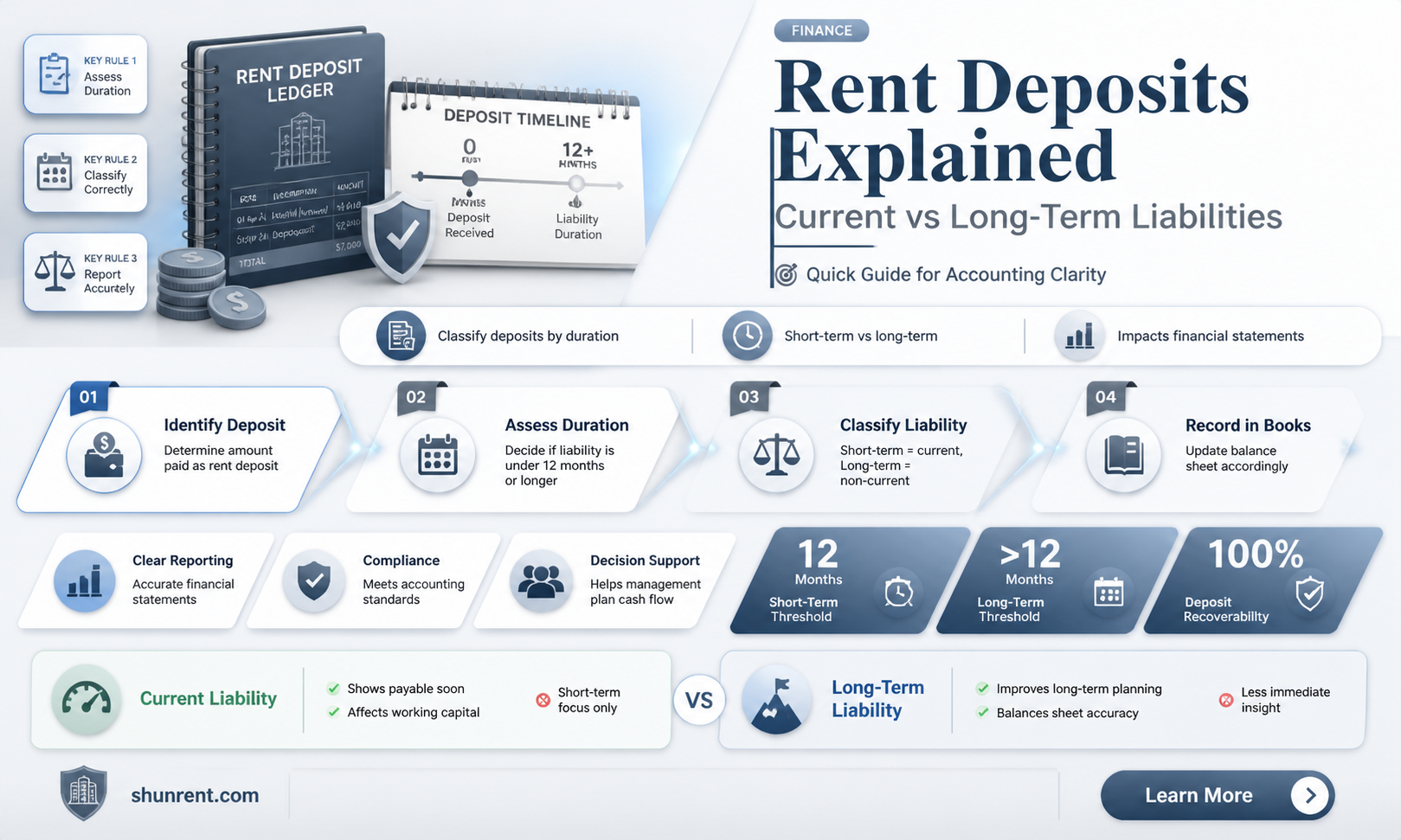

Rent deposits, often a point of contention between landlords and tenants, are subject to classification criteria that determine their treatment as current or long-term assets or liabilities. The primary factor in this classification is the expected duration of the deposit's restriction. If a deposit is expected to be returned within 12 months or one operating cycle, whichever is longer, it is typically classified as a current asset or liability. For instance, a security deposit held by a landlord for a one-year lease would generally be considered a current liability, as it is expected to be returned at the end of the lease term.

Classification Steps and Considerations

To accurately classify rent deposits, follow these steps: (1) Determine the lease term and any renewal options; (2) Assess the likelihood of deposit return based on lease conditions and historical data; (3) Evaluate the deposit's restriction period, considering both time and operating cycle constraints. For example, a deposit held for a 10-month lease with a high probability of return would be classified as current, whereas a deposit for a 15-month lease might be considered long-term if the return is not expected within 12 months.

Comparative Analysis of Deposit Types

Different types of deposits may have varying classification criteria. Security deposits, which are typically refundable, are more likely to be classified as current liabilities. In contrast, non-refundable deposits, such as lease initiation fees, may be treated as long-term liabilities or even revenue, depending on the specific circumstances and accounting standards applied. For instance, under ASC 842, non-refundable lease payments may be recognized as revenue over the lease term, whereas refundable deposits would be classified as liabilities.

Practical Tips for Accurate Classification

When classifying rent deposits, consider the following practical tips: (a) Review lease agreements thoroughly to understand deposit terms and conditions; (b) Maintain detailed records of deposit transactions, including amounts, dates, and return expectations; (c) Consult accounting standards, such as ASC 842 or IFRS 16, for guidance on deposit classification. Additionally, be mindful of jurisdictional requirements, as local laws may dictate specific treatment of rent deposits. For example, some states require landlords to hold security deposits in escrow accounts, which may impact their classification.

Cautions and Common Pitfalls

Misclassification of rent deposits can lead to financial misstatements and compliance issues. Common pitfalls include: (i) Failing to reassess deposit classification upon lease renewal or modification; (ii) Overlooking the impact of operating cycle length on current/long-term classification; (iii) Inconsistently applying accounting standards across similar deposits. To avoid these errors, establish clear policies and procedures for deposit classification, provide regular training to accounting staff, and conduct periodic reviews of deposit accounts to ensure accuracy and compliance. By following these guidelines, organizations can accurately classify rent deposits, maintaining financial integrity and adhering to regulatory requirements.

Berkeley Renters' Rights: Current Status and Housing Challenges Explained

You may want to see also

Explore related products

![]()

Lease Term Impact

The duration of a lease agreement significantly influences how rent deposits are classified on financial statements. Short-term leases, typically under one year, often treat rent deposits as current liabilities or assets, reflecting their immediate nature. Conversely, long-term leases, spanning multiple years, may categorize these deposits as long-term liabilities or assets, aligning with the extended commitment. This classification isn’t arbitrary; it directly impacts liquidity ratios and financial health assessments. For instance, a 12-month lease deposit would appear under current liabilities, while a 5-year lease deposit would shift to the long-term section, providing a clearer picture of short-term obligations versus long-term commitments.

Consider a small business signing a 3-year lease for office space. The $10,000 security deposit, if refundable, would initially be recorded as a long-term asset, gradually reclassified to current as the lease nears expiration. This reclassification ensures accuracy in financial reporting, as the deposit transitions from a long-term hold to an imminent return. Similarly, landlords must mirror this treatment, moving the deposit from long-term liabilities to current as the lease term shortens. Failure to adjust classifications can misrepresent financial stability, misleading investors or stakeholders about available liquid assets.

From a practical standpoint, businesses should establish a systematic process for tracking lease terms and deposit reclassifications. For example, using accounting software with automated reminders can ensure deposits are reclassified from long-term to current in the final year of a lease. Additionally, maintaining detailed lease schedules, including deposit amounts, lease durations, and renewal options, can prevent oversight. For leases with renewal options, deposits should remain classified as long-term until the option is exercised or expires, as the commitment remains open-ended.

A comparative analysis reveals that industries with frequent short-term leases, such as retail pop-up stores, predominantly classify deposits as current. In contrast, sectors like manufacturing, often tied to multi-year leases for specialized facilities, treat deposits as long-term. This industry-specific approach highlights the importance of aligning financial reporting with operational realities. For instance, a retailer with a 6-month lease would prioritize current liability management, while a manufacturer with a 10-year lease would focus on long-term financial planning.

In conclusion, the lease term dictates whether rent deposits are current or long-term, with direct implications for financial accuracy and strategic planning. Businesses must adopt proactive measures, such as automated tracking and detailed lease schedules, to ensure proper classification. By understanding this relationship, companies can maintain transparent financial statements, accurately reflecting their short-term liquidity and long-term obligations. This precision not only aids internal decision-making but also fosters trust with external stakeholders.

Is Renting a Scooter in Berlin Worth It for Touring?

You may want to see also

Explore related products

![Adams Residential Lease, Forms and Instructions [Print and Downloadable] (LF310)](https://m.media-amazon.com/images/I/81uP3OCk9qL._AC_UY218_.jpg)

![]()

Accounting Standards

Rent deposits present a classification conundrum in financial reporting, hinging on the interpretation of accounting standards. The International Financial Reporting Standards (IFRS) and Generally Accepted Accounting Principles (GAAP) offer guidance, but nuances exist. IFRS, under IAS 37, classifies provisions, contingent liabilities, and contingent assets, emphasizing the timing and probability of outflow. A rent deposit, if refundable and held for a specific future period, might be considered a non-current asset, as it’s not expected to be realized within the next 12 months. Conversely, GAAP, particularly ASC 420, focuses on the nature of the deposit and the contractual terms. If the deposit is held for the duration of a long-term lease, it could be classified as non-current, aligning with the lease term’s longevity. However, if the deposit is refundable upon short notice or tied to annual renewals, it may be treated as current. The key lies in the substance of the agreement, not just its form, requiring careful analysis of the deposit’s purpose and expected return timeline.

To navigate this classification, accountants must scrutinize lease agreements for specific clauses. For instance, a deposit held as security for damages or unpaid rent typically aligns with the lease term. If the lease spans multiple years, the deposit should mirror this duration, classifying it as non-current. However, deposits tied to annual inspections or short-term obligations may warrant current classification. Practical tip: Review the lease agreement for refund conditions, holding periods, and termination clauses. If the deposit is earmarked for return at the end of a multi-year lease, treat it as non-current. Conversely, if it’s refundable annually or upon demand, classify it as current. This approach ensures compliance with accounting standards while reflecting the economic reality of the arrangement.

A comparative analysis of IFRS and GAAP reveals subtle differences in treatment. Under IFRS, the focus is on the *substance* of the deposit—whether it’s held for a specific future purpose. GAAP, however, leans toward the *legal form*, emphasizing contractual terms. For example, a five-year lease deposit under IFRS would likely be non-current, as it’s tied to the lease’s duration. Under GAAP, if the contract specifies annual renewals, the deposit might be classified as current, despite the longer lease term. This divergence underscores the importance of aligning classification with the standard being applied. Accountants operating in dual-reporting environments must reconcile these differences, often through detailed disclosures or policy elections, to ensure transparency and comparability.

Persuasively, the classification of rent deposits as current or non-current impacts financial ratios and stakeholder perceptions. Misclassification can distort liquidity metrics, such as the current ratio, misleading investors about a company’s short-term financial health. For instance, a non-current deposit incorrectly classified as current artificially inflates current assets, overstating liquidity. Conversely, a current deposit classified as non-current understates immediate resources. To mitigate this, accountants should adopt a conservative approach, erring on the side of current classification when in doubt. Additionally, documenting the rationale for classification—including lease terms, refund conditions, and standard references—provides an audit trail and supports defensible reporting. This practice not only ensures compliance but also fosters trust in financial statements.

Instructively, classifying rent deposits requires a systematic approach. Step one: Identify the deposit’s purpose and refund conditions from the lease agreement. Step two: Determine the expected holding period—is it tied to a long-term lease or subject to annual review? Step three: Apply the relevant accounting standard, considering both the substance and form of the arrangement. Caution: Avoid relying solely on the lease term; assess refund triggers and holding obligations. For example, a 10-year lease deposit with annual refund options should be treated as current, despite the lease’s duration. Conclusion: Consistent application of these steps ensures accurate classification, aligning financial reporting with economic reality and accounting standards.

Rent-A-Center Marianna, Florida: Closing Time and Store Hours

You may want to see also

Explore related products

![]()

Refund Conditions

Rent deposits, often a point of contention between landlords and tenants, are typically classified as current liabilities on a landlord's balance sheet. This classification stems from the expectation that the deposit will be refunded within a year, aligning with the definition of current liabilities. However, the conditions under which a deposit is refunded can significantly impact this categorization. For instance, if a lease agreement stipulates that the deposit is non-refundable under certain conditions, it might be argued that a portion of the deposit could be considered long-term, especially if those conditions are likely to be met over an extended period.

From a legal perspective, refund conditions must comply with local tenant laws, which often dictate the maximum deposit amount, allowable deductions, and the refund timeline. For instance, in California, landlords must return the deposit within 21 days after lease termination, while in New York, the timeframe is 14 days. Failure to comply can result in penalties, such as the landlord forfeiting the right to withhold any portion of the deposit. Tenants should familiarize themselves with these laws to ensure their rights are protected and to challenge unfair deductions effectively.

A comparative analysis reveals that refund conditions can vary widely based on geographic location and property type. Commercial leases, for example, often have more stringent conditions, including clauses for restoring the property to its original condition, which can be costly. In contrast, residential leases may focus more on cleanliness and minor repairs. Understanding these differences is crucial for both landlords and tenants to set realistic expectations and avoid financial surprises. For landlords, drafting clear, enforceable refund conditions can reduce legal risks and improve tenant relations.

Practically, tenants can take proactive steps to maximize their deposit refund. These include conducting a pre-moveout inspection with the landlord, addressing minor repairs independently, and ensuring all rent payments are up to date. Landlords, on the other hand, should provide itemized deductions with receipts for any expenses incurred. By fostering transparency and communication, both parties can navigate refund conditions more smoothly. Ultimately, while rent deposits are generally treated as current liabilities, the specific refund conditions can introduce complexities that require careful management and adherence to legal standards.

Rent Comerica Park: Your Ultimate Guide to Playing a Game

You may want to see also

Explore related products

![Method of Administering Leases of Iron-Ore Deposits Belonging to the State of Minnesota 1919 [Leather Bound]](https://m.media-amazon.com/images/I/617DLHXyzlL._AC_UY218_.jpg)

![]()

Financial Reporting Treatment

Rent deposits present a nuanced challenge in financial reporting, primarily due to their classification as current or long-term liabilities. Under International Financial Reporting Standards (IFRS) and Generally Accepted Accounting Principles (GAAP), the treatment hinges on the deposit’s nature and the lease agreement’s terms. If the deposit is refundable within 12 months or the operating cycle, it is classified as a current liability. Conversely, if the refund is expected beyond this period, it is treated as a long-term liability. For example, a security deposit held by a landlord for a 10-year lease, refundable at termination, would typically be recorded as a long-term liability unless specific conditions dictate otherwise.

The analytical approach to classifying rent deposits requires a deep dive into the lease agreement’s fine print. Key factors include the deposit’s purpose (e.g., security vs. advance payment), refund conditions, and the lessee’s control over the funds. For instance, if a tenant can apply the deposit toward the final month’s rent, it may be treated as a prepaid expense rather than a liability. Accountants must also consider the substance over form principle, ensuring the financial statements reflect the economic reality of the arrangement, not just its legal structure.

From a practical standpoint, misclassification of rent deposits can distort liquidity ratios and mislead stakeholders. To avoid this, follow these steps: first, review the lease agreement to identify refund terms and conditions. Second, assess the deposit’s expected refund timeline relative to the reporting period. Third, consult accounting standards (e.g., ASC 842 under GAAP or IFRS 16) for specific guidance. For example, a $50,000 deposit on a 5-year lease, refundable at the end, should be recorded as a long-term liability, with a corresponding footnote disclosing the arrangement’s details.

A comparative analysis reveals inconsistencies in practice, particularly between industries. Real estate companies often classify rent deposits as long-term liabilities due to extended lease terms, while retail tenants may treat them as current if refunds are tied to short-term conditions. This disparity underscores the importance of industry-specific guidelines and consistent application. For instance, a tech startup with a 2-year lease might classify its deposit as current, while a manufacturing firm with a 20-year lease would categorize it as long-term, reflecting their differing operational cycles.

In conclusion, the financial reporting treatment of rent deposits demands meticulous attention to detail and adherence to accounting standards. By focusing on the lease agreement’s terms, refund conditions, and economic substance, organizations can ensure accurate classification. This not only enhances the reliability of financial statements but also fosters transparency and trust among investors and stakeholders. For example, a footnote explaining the classification rationale can provide clarity, such as: “Rent deposits of $200,000 are classified as long-term liabilities as they are refundable upon lease termination in 2030.” Such specificity bridges the gap between technical accounting and practical understanding.

Exploring 4250 El Camino Real: Palo Alto Rent and Residents

You may want to see also

Frequently asked questions

Rent deposits are typically classified as long-term assets if they are not expected to be returned within the next 12 months. However, if the deposit is refundable within a year, it may be categorized as a current asset.

Determine the expected refund timeline. If the deposit is refundable within 12 months, it is current. If it extends beyond 12 months, it is long-term.

Yes, if the terms of the lease change and the deposit becomes refundable within 12 months, it can be reclassified from long-term to current.

No, treatment depends on the lease agreement and refund terms. Some deposits may be expensed immediately, while others are capitalized as assets.

If classified as a current asset, it increases current assets. If long-term, it increases non-current assets. Both reflect the company’s right to recover the deposit.