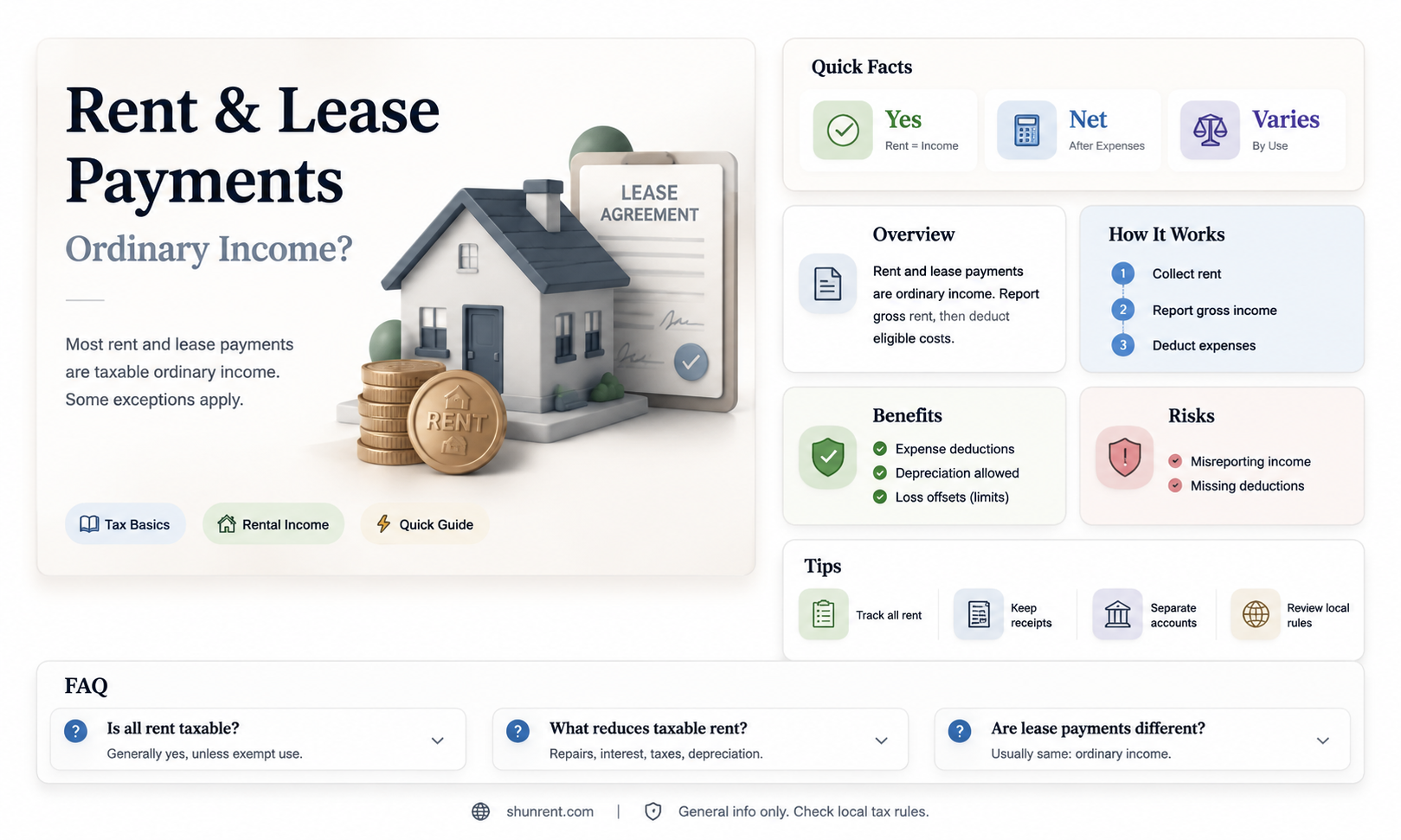

Rent or lease payments are generally considered ordinary income. The IRS defines rental income as any payment for the use or occupation of property. This includes normal rent payments, advance rent, lease termination payments, and lease inducement payments. However, there are certain expenses that landlords can deduct from this income, such as mortgage interest, property tax, repairs, advertising, and maintenance. These deductions can reduce the amount of rental income that is taxed as ordinary income. It's important to note that rental income is typically taxed as passive income, similar to stock dividends or real estate investment trust distributions, and the specific tax treatment may vary depending on an individual's circumstances.

Explore related products

![Adams Residential Lease, Forms and Instructions [Print and Downloadable] (LF310)](https://m.media-amazon.com/images/I/81uP3OCk9qL._AC_UL320_.jpg)

What You'll Learn

![]()

Rent payments are taxed as ordinary income

Rental income can include various types of payments beyond normal rent payments. For example, advance rent, which is any amount received before the period it covers, must be included in rental income for the year it is received. Lease termination payments received by the landlord are also taxable income, as they are considered a substitute for rental payments. If a tenant performs services, such as landscaping or repairs, in exchange for rent or a rent reduction, the value of those services is also considered rental income. Additionally, if a landlord withholds a refund of a tenant's security deposit, that amount is included in rental income.

There are also certain expenses that can be deducted from rental income. These may include mortgage interest, property tax, operating expenses, depreciation, repairs, advertising, maintenance, utilities, and insurance. By properly documenting these expenses, landlords may be able to reduce the amount of rental income subject to tax.

It is important to note that the tax treatment of rental income can vary depending on whether the rental activity is considered a business or an investment. Landlords who work regularly and continuously in their rental business may be eligible for substantial deductions. Additionally, the tax rules and regulations can change over time, so it is always advisable to refer to the latest guidelines provided by official sources, such as the IRS.

Rent and Utilities: How Much of Your Income?

You may want to see also

Explore related products

![]()

Advance rent and security deposits

Rent payments are generally considered ordinary income. However, there are some nuances to this, particularly when it comes to advance rent and security deposits.

Advance rent refers to any amount received by the landlord before the period it covers. For example, if a tenant pays rent for the first six months of a lease upfront, this would be considered advance rent. Advance rent is typically non-refundable and is applied towards the rent for the specified timeframe in the lease or rental agreement. It is considered taxable income for the landlord in the year it is received, regardless of the period covered or the accounting method used. This means that if a landlord receives advance rent in December for the first six months of a lease starting in January, they must report the full amount as income for the year they received it (December) rather than the year the tenant occupies the property.

Security deposits, on the other hand, are upfront payments made by tenants to cover potential damages or violations of the lease. Unlike advance rent, security deposits are typically refundable if not used, and landlords are required to return them to tenants at the end of the lease, minus any deductions for damages. Security deposits are not considered taxable income when received. They are only taxed if and when the landlord is no longer obligated to return them to the tenant, such as in the case of damages or early lease cancellation.

It is important to note that the distinction between advance rent and security deposits is not always clear-cut. Some leases may label a payment as a "security deposit" when it functions as an advance rental payment. In such cases, the description of how the funds will be used is more important than the label. If a payment is intended to cover future rental payments, it is considered advance rent and is taxable upon receipt.

Landlords should be aware of local and state laws that regulate security deposits and advance rent payments. For example, some states limit the number of months' rent that can be paid in advance or require interest to be paid on security deposits. It is crucial to understand the legal requirements and tax implications before accepting advance rent or security deposits from tenants.

Boat Rentals: What You Need to Know

You may want to see also

Explore related products

![]()

Lease termination payments

From the lessee's perspective, termination penalties are typically allocated to the remaining lease components, and subsequent accounting depends on the classification of these components. If the lessee surrenders control of a portion of the leased space, it is considered a partial termination. In this case, the lease liability is reassessed based on the terms of the modified lease. The lessee would then adjust the lease liability to match the present value of the remaining future lease payments, including any termination penalties.

From the lessor's perspective, the taxation of lease termination payments has been a point of contention between taxpayers and the IRS. The primary question revolves around whether the payment can be immediately expensed as an ordinary and necessary business expense or if it must be capitalized and recovered over time. IRS regulations effective in 2003 generally require the capitalization of amounts paid by a lessor to a lessee to terminate a lease of real or tangible personal property. However, the regulations do not explicitly address how the capitalized costs should be recovered.

One approach to cost recovery is based on case law, specifically the Ninth Circuit's analysis in Handlery Hotels, Inc. in 1981. The court concluded that a lessor's capitalized termination costs should generally be amortized over the remaining term of the lease. However, the court also identified exceptions to this principle, such as when the lessor makes a termination payment to demolish an existing structure and build a new one or make extensive improvements to the property. Additionally, in the case of Wells Fargo Bank & Union Trust Co. in 1947, the court held that the amortization period for the lease termination payment was the term of the new lease when the lessor terminated the old lease to enter into a new one with higher lease payments.

Collecting Unpaid Rent: What to Do When Tenants Skip Out

You may want to see also

Explore related products

![]()

Landlord deductions

If you are a landlord, you must include all the rent you receive as gross income on your tax return. This includes advance rent payments, lease payments with an option to buy, lease cancellation payments, and certain security deposits. However, there are several federal tax deductions available for landlords that can help reduce your tax burden. These include:

- Mortgage interest: Landlords can deduct mortgage interest as a rental expense. This is usually the biggest deduction.

- Property tax: You can deduct property taxes from your rental income.

- Operating expenses: Costs associated with operating your rental property, such as advertising and utilities, may be deductible.

- Depreciation: You can recover some or all of the costs of improvements to your rental property through depreciation. This includes items used in your rental business, which can be depreciated at a faster rate.

- Repairs and maintenance: The costs of repairing and maintaining your rental property to keep it in good condition are generally deductible in the tax year you pay for them.

- Travel expenses: If you need to travel long distances to check on your property, you may be able to deduct the cost of travel, including gas, oil, lease payments, repairs, and parking.

- Professional services: Costs for professional services, such as legal or accounting advice, may be deductible.

- Eviction-related fees: Any fees associated with eviction proceedings may be deductible.

- Insurance premiums: You can deduct the cost of insurance premiums for your rental property.

It is important to note that deductions are generally made in the year the expense is paid and that you should keep tidy records of all expenses to claim them on your tax return.

Bobby and Giada: Cooking Up Romance?

You may want to see also

Explore related products

![]()

Tenant allowances

Tenant improvement allowances can be structured in different ways:

- Fixed Amount: The landlord offers a predetermined sum to cover the tenant's eligible expenses. This amount typically ranges from 25% to 150% of the total first year's rental payments, depending on factors such as the condition and age of the space.

- Per-Square-Foot Basis: The TIA is calculated based on a per-square-foot allowance, which is then multiplied by the total square footage of the leased space.

- Reimbursement Arrangement: In some cases, the tenant may initially pay for the improvements and then seek reimbursement from the landlord. This arrangement requires careful management of payments and cash flow.

It is important to note that tenant improvement allowances are not considered rental income by the tenant. Instead, they are treated as lease incentives, reducing the rent expense over the lease term. On the other hand, when the landlord bears the cost of improvements, the TIA is recorded as an incentive or inducement on the tenant's balance sheet, effectively reducing their overall occupancy cost.

Renting a U-Haul: A Quick Guide to Daily Rentals

You may want to see also

Frequently asked questions

Yes, rent or lease payments are considered ordinary income. Rental income is defined by the IRS as "any payment for the use or occupation of property" and is generally taxed as ordinary income.

Rental income includes any payment received for the use or occupation of property, including normal rent payments, advance rent, lease termination payments, and security deposits used as final rent payments. It also includes any services or property received in lieu of rent, valued at their fair market value.

Several expenses can be deducted from rental income, including mortgage interest, property tax, operating expenses, depreciation, repairs, advertising, maintenance, utilities, and insurance. These expenses must be reasonable, ordinary, and necessary for the business.