Rent on the statement of cash flows is a critical component of a company's financial reporting, reflecting the cash outflows associated with leasing property or equipment. It is typically classified under operating activities, as it represents a regular expense incurred in the course of business operations. This line item provides insight into a company's liquidity and its ability to meet short-term obligations, as rent payments are often a significant and recurring cash outflow. Properly accounting for rent ensures transparency and helps stakeholders understand the financial health and operational efficiency of the business.

| Characteristics | Values |

|---|---|

| Definition | Rent on the statement of cash flows refers to the cash payments made by a company for the use of leased property or equipment. It is classified under operating activities. |

| Classification | Operating Activity |

| Reporting Standard | Under both IFRS (International Financial Reporting Standards) and GAAP (Generally Accepted Accounting Principles), rent payments are reported as cash outflows from operating activities. |

| Purpose | Reflects the ongoing cost of using leased assets in the normal course of business operations. |

| Frequency | Typically reported periodically (e.g., monthly, quarterly, annually) based on lease agreements. |

| Impact on Cash Flow | Reduces cash balance as it represents a cash outflow. |

| Distinction from Capital Expenditure | Unlike capital expenditures, rent is not an investment in long-term assets but a recurring operational expense. |

| Disclosure | May be explicitly listed as "Rent Paid" or included under "Other Operating Expenses" depending on materiality and company policy. |

| Relevance | Provides insight into a company's operational efficiency and liquidity, especially for businesses heavily reliant on leased assets. |

| Example | If a company pays $10,000 monthly for office rent, this amount is deducted from operating cash flow. |

Explore related products

What You'll Learn

- Rent Classification: Distinguishes operating vs. financing rent payments based on lease type and terms

- Operating Leases: Rent expenses reported under operating activities as cash outflow

- Finance Leases: Rent payments split into interest and principal, affecting cash flow

- Prepaid Rent: Adjustments for rent paid in advance on the cash flow statement

- Lease Incentives: Impact of landlord incentives on rent expense and cash flow reporting

![]()

Rent Classification: Distinguishes operating vs. financing rent payments based on lease type and terms

Rent classification is a critical step in accurately reflecting lease obligations on a statement of cash flows, ensuring that payments are categorized as either operating or financing activities based on the nature of the lease. This distinction hinges on whether the lease is classified as an operating lease or a finance lease under accounting standards like ASC 842 or IFRS 16. Operating leases are treated as rental agreements, with payments recorded as operating cash outflows. In contrast, finance leases are akin to purchasing the asset, with payments split between interest (operating activity) and principal repayment (financing activity). Misclassification can distort a company’s financial health, making it appear either more operationally efficient or less leveraged than it truly is.

To classify rent payments correctly, examine the lease terms and the economic substance of the agreement. Key indicators of a finance lease include a lease term covering most of the asset’s useful life, the presence of a bargain purchase option, or lease payments totaling the asset’s fair value. For example, a 10-year lease on a piece of machinery with a 12-year useful life and a $1 purchase option at the end would likely be classified as a finance lease. In such cases, separate the cash flow into interest (operating) and principal (financing) components using the effective interest rate method. Operating leases, on the other hand, are straightforward: rent payments are fully reported under operating activities, as seen in short-term office space rentals with no transfer of ownership.

Practical application of rent classification requires meticulous documentation and consistent application of accounting policies. Companies should maintain a lease inventory detailing each lease’s terms, classification, and payment schedule. For instance, a retail chain with 50 store leases must assess each one individually, as some may qualify as finance leases while others remain operating leases. Tools like lease accounting software can automate the separation of interest and principal for finance leases, reducing the risk of errors. Regular reviews of lease agreements, especially at renewal or modification, ensure ongoing compliance with classification criteria.

The implications of proper rent classification extend beyond compliance, influencing financial ratios and stakeholder perceptions. For instance, misclassifying a finance lease as operating can artificially lower the debt-to-equity ratio, misleading investors about leverage risk. Conversely, accurate classification provides a clearer picture of cash flow sustainability and capital structure. Consider a tech startup leasing equipment under a finance lease: reporting principal repayments as financing activities highlights its investment in long-term assets, whereas lumping all payments under operating activities might obscure its growth strategy. Thus, precision in rent classification is not just an accounting detail but a strategic communication tool.

In conclusion, distinguishing between operating and financing rent payments demands a nuanced understanding of lease terms and accounting principles. By focusing on the economic substance of the lease and employing systematic documentation practices, companies can ensure their statement of cash flows accurately reflects their financial obligations. This clarity not only meets regulatory requirements but also enhances transparency, enabling stakeholders to make informed decisions about the company’s operational efficiency and financial stability.

Understanding Ground Rent Registration in Baltimore City: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Operating Leases: Rent expenses reported under operating activities as cash outflow

Rent expenses from operating leases are a critical component of the statement of cash flows, specifically under operating activities. These expenses represent the cash outflows a company incurs to lease assets like property, equipment, or vehicles without transferring ownership. Unlike financing activities, which involve long-term debt or equity transactions, operating leases are treated as day-to-day business expenses, reflecting the company’s ability to generate cash from core operations. For instance, a retail chain leasing storefronts would report these payments as operating cash outflows, signaling ongoing operational costs rather than capital investments.

Analyzing rent expenses in this context requires understanding the distinction between operating and financing leases under accounting standards like ASC 842 or IFRS 16. Operating leases are not capitalized on the balance sheet; instead, rent payments are expensed directly on the income statement and reflected as cash outflows in the operating section of the cash flow statement. This treatment aligns with the principle that these leases are short-term in nature and do not confer ownership rights. For example, a tech startup leasing office space for a 3-year term would report monthly rent payments as operating cash outflows, avoiding the complexity of asset and liability recognition.

From a practical standpoint, investors and analysts scrutinize rent expenses under operating activities to assess a company’s liquidity and operational efficiency. High rent outflows relative to revenue may indicate over-reliance on leased assets or inefficient cost management. Conversely, stable rent expenses can signal a well-managed operational structure. For instance, a restaurant chain with consistent rent payments across multiple locations demonstrates predictable cash outflows, which is favorable for cash flow forecasting. To optimize this, companies should negotiate flexible lease terms, such as rent escalation caps or termination clauses, to mitigate future cash flow risks.

A comparative analysis of rent expenses across industries highlights their variability. Retailers and hospitality businesses often face higher rent outflows due to prime location requirements, while manufacturing firms may prioritize leased equipment to preserve capital. For example, a clothing retailer might allocate 15-20% of its operating cash flows to rent, whereas a software company could spend less than 5%. This disparity underscores the importance of benchmarking rent expenses within industry norms to evaluate financial health accurately. Tools like cash flow ratios (e.g., rent-to-revenue) can provide actionable insights for stakeholders.

In conclusion, rent expenses from operating leases serve as a barometer of a company’s operational sustainability and cash flow management. By reporting these outflows under operating activities, financial statements offer transparency into recurring costs that impact liquidity. Companies should monitor these expenses closely, leveraging lease agreements strategically to balance operational needs with financial stability. For investors, understanding this line item is essential for evaluating a company’s ability to generate cash from its core business, free from the distortions of non-operating activities.

How to Transfer RentSpree Applications to Another Real Estate Agent

You may want to see also

Explore related products

![]()

Finance Leases: Rent payments split into interest and principal, affecting cash flow

Rent payments under finance leases are not straightforward expenses; they are hybrid transactions that blend interest and principal repayment. This duality is critical for accurate cash flow reporting. When a company records a rent payment, it must allocate a portion to interest expense—reflecting the cost of borrowing—and the remainder to reducing the lease liability, akin to paying down a loan. For instance, in the first year of a $12,000 annual lease with a 5% interest rate and a $100,000 present value, approximately $5,000 would be interest, while $7,000 reduces the principal. This split ensures the statement of cash flows reflects both the financing and operating aspects of the lease.

The allocation of rent payments into interest and principal directly impacts the cash flow statement’s structure. Interest payments are classified under operating activities as part of cash outflows from operations, while principal repayments are often reported under financing activities, mirroring the repayment of debt. This distinction is particularly important under accounting standards like ASC 842 or IFRS 16, which require leases to be capitalized on the balance sheet. Misclassification can distort a company’s operating cash flow, making it appear weaker or stronger than reality. For example, a $10,000 rent payment with $2,000 in interest and $8,000 in principal would show $2,000 in operating cash outflows and $8,000 in financing cash outflows.

To accurately handle finance lease payments, follow these steps: first, calculate the interest portion using the lease liability’s opening balance and the interest rate. Second, subtract the interest from the total payment to determine the principal reduction. Third, record the interest in the operating section and the principal in the financing section of the cash flow statement. Tools like Excel or accounting software can automate these calculations, reducing errors. For instance, the formula `=Lease Liability * Interest Rate` can compute monthly interest. Always reconcile the lease liability balance to ensure accuracy, as discrepancies can lead to misstated financial statements.

A common pitfall is treating rent payments as a single operating expense, which ignores the financing component. This approach understates interest expenses and overstates operating cash flows, misleading stakeholders about the company’s financial health. Another error is inconsistently applying the interest rate, especially when it’s variable. To avoid these mistakes, maintain a detailed lease schedule tracking the interest rate, payment dates, and remaining liability. Regularly review the schedule to ensure alignment with accounting standards and provide transparency in financial reporting.

In conclusion, the split of rent payments into interest and principal under finance leases is a nuanced yet essential aspect of cash flow reporting. It requires meticulous calculation, proper classification, and adherence to accounting standards. By understanding and correctly applying these principles, companies can present a more accurate picture of their cash flows, aiding investors, creditors, and management in making informed decisions. This approach not only ensures compliance but also enhances the credibility of financial statements.

Late Rent in Arizona: What Are Your Rights?

You may want to see also

Explore related products

![]()

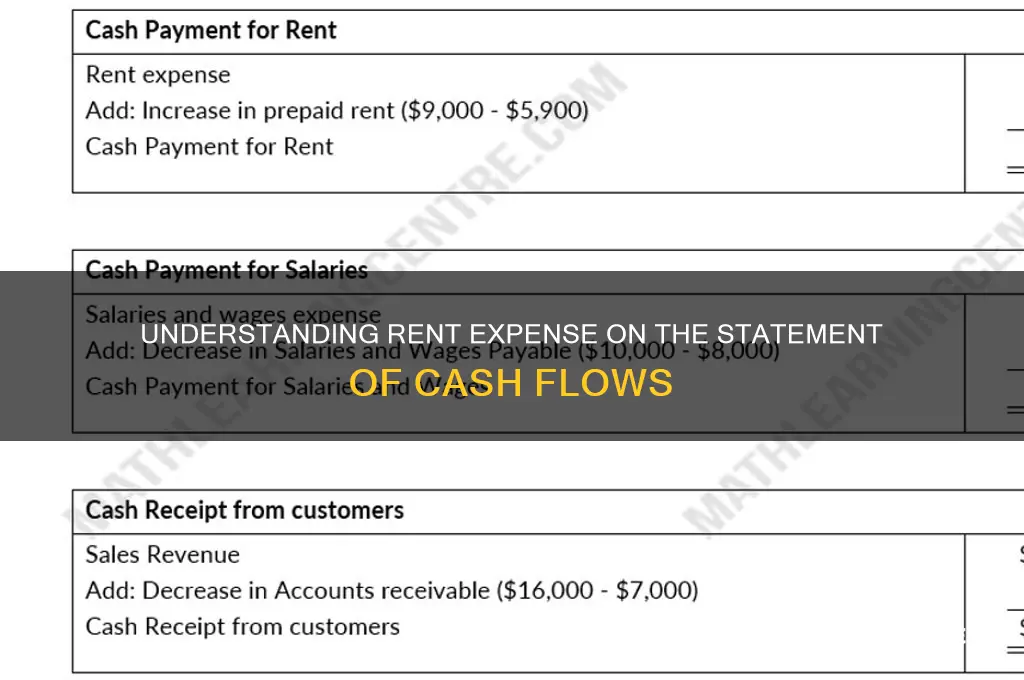

Prepaid Rent: Adjustments for rent paid in advance on the cash flow statement

Prepaid rent represents a unique challenge in cash flow reporting because it distorts the timing of cash outflows relative to expense recognition. When a company pays rent in advance, the entire cash payment is recorded in the period it occurs, but the expense is allocated over the rental period. This mismatch creates a temporary difference between cash flow and income statement treatment, requiring adjustment to accurately reflect operating activities.

Consider a scenario where a company pays $12,000 annually for office space in January but recognizes $1,000 as rent expense each month. On the income statement, only $1,000 appears monthly, but the cash flow statement initially shows a $12,000 outflow in January. Without adjustment, this overstates January’s cash outflow and understates it in subsequent months. To correct this, the prepaid rent account is adjusted on the cash flow statement. The $12,000 payment is added back to operating cash flow in January, and $1,000 is subtracted monthly as the expense is recognized, ensuring cash flow aligns with the actual timing of cash usage.

Adjusting for prepaid rent is critical for investors and analysts assessing a company’s liquidity and operational efficiency. For instance, a tech startup with significant prepaid rent might appear cash-poor in the short term due to a large initial outflow. However, adjusting for prepaid rent reveals a more sustainable cash position, as the expense is spread over time. Conversely, a company with minimal prepaid rent adjustments may face uneven cash flow, signaling poor financial planning or short-term lease commitments.

To implement this adjustment, follow these steps: first, identify the prepaid rent balance at the beginning and end of the period. Next, calculate the change in prepaid rent (ending balance minus beginning balance). If the change is positive, subtract it from operating cash flow, as more rent was prepaid during the period. If negative, add it back, as prepaid rent was expensed. Finally, ensure the adjustment aligns with the indirect method of cash flow reporting, where non-cash items and changes in working capital are reconciled to net income.

In practice, companies often use accounting software to automate these adjustments, but manual review is essential to catch errors. For example, a miscalculated prepaid rent balance could lead to overstated or understated cash flow, misleading stakeholders. Regularly reconciling prepaid rent accounts and cross-referencing lease agreements ensures accuracy. By mastering prepaid rent adjustments, financial professionals can provide a clearer picture of a company’s cash flow dynamics, fostering better decision-making and transparency.

Phone Dies During Bike Rental? Quick Solutions to Stay on Track

You may want to see also

Explore related products

![]()

Lease Incentives: Impact of landlord incentives on rent expense and cash flow reporting

Landlord incentives, such as rent-free periods or tenant improvement allowances, significantly alter the financial reporting of lease agreements. These incentives effectively reduce the lessee’s future cash outflows but require specific accounting treatment to reflect their economic impact accurately. Under accounting standards like ASC 842 or IFRS 16, lease incentives are not directly subtracted from rent expense in the period received. Instead, they are amortized over the lease term, reducing the right-of-use asset and lease liability systematically. This treatment ensures that the rent expense reported each period aligns with the economic benefit derived from the lease, rather than the actual cash payments made.

Consider a practical example: a tenant signs a 10-year lease with a one-year rent-free period as an incentive. While no cash is paid in the first year, the tenant must recognize a straight-line rent expense over the entire lease term. This means a portion of the incentive is effectively deferred and reduces rent expense annually, rather than being fully recognized upfront. From a cash flow perspective, the rent-free period improves operating cash flows in the initial year, but the straight-line expense method smooths out the impact on the income statement, providing a more consistent view of lease costs over time.

The interplay between lease incentives and cash flow reporting is critical for financial analysis. Investors and stakeholders must distinguish between the timing of cash payments and the recognition of rent expense. For instance, a sudden spike in operating cash flows due to a rent-free period might misleadingly suggest improved operational efficiency, when in reality, it reflects a temporary lease incentive. Conversely, the straight-line rent expense method ensures that financial statements reflect the lease’s true cost, even if cash outflows are deferred. This distinction is particularly important in industries like retail or hospitality, where lease incentives are common and can materially impact financial ratios.

To navigate these complexities, companies should adopt a structured approach. First, identify all lease incentives within the agreement and quantify their total value. Second, determine the appropriate amortization period, typically the lease term, to spread the incentive’s benefit. Third, reconcile the difference between cash payments and rent expense in the statement of cash flows, often under “operating activities.” For example, if a tenant pays $100,000 annually but recognizes $120,000 in rent expense due to a prior incentive, the $20,000 difference would be added back to operating cash flows. This ensures transparency and aligns with accounting standards.

In conclusion, lease incentives from landlords have a dual impact on rent expense and cash flow reporting. While they improve short-term liquidity, their accounting treatment requires careful amortization to reflect the lease’s economic reality. By understanding these mechanics, businesses can accurately interpret financial statements and communicate the true financial implications of lease agreements to stakeholders. Practical steps, such as detailed lease documentation and consistent application of accounting policies, are essential to avoid misstatements and ensure compliance with reporting standards.

Discover Malta's Top Rental Areas for Expat Living and Locals

You may want to see also

Frequently asked questions

Rent on the statement of cash flows refers to the cash payments made by a company for leasing property, equipment, or other assets. It is typically classified under operating activities as it represents a regular operating expense.

Rent is usually classified under operating activities on the statement of cash flows because it is considered a core part of a company’s day-to-day operations, similar to other operating expenses like wages or utilities.

Not necessarily. The rent expense on the income statement is an accrual-based figure, while the rent on the statement of cash flows reflects actual cash payments made during the period. Differences may arise due to timing of payments or prepaid rent.

![Rent [Blu-ray]](https://m.media-amazon.com/images/I/61gNC08X3PL._AC_UY218_.jpg)

![Rent [DVD]](https://m.media-amazon.com/images/I/516CgH-EDLL._AC_UY218_.jpg)

![Rent: Filmed Live on Broadway [Blu-ray]](https://m.media-amazon.com/images/I/51SDxJNQfVL._AC_UY218_.jpg)

![Rent (Blu-ray) Starring Rosario Dawson, Taye Diggs, Jesse L. Martin, Idina Menzel [Spanish Artwork]](https://m.media-amazon.com/images/I/81wUIoGBEcL._AC_UY218_.jpg)

![RENT (Original Motion Picture Soundtrack) [Explicit]](https://m.media-amazon.com/images/I/81reolbqVvL._AC_UY218_.jpg)