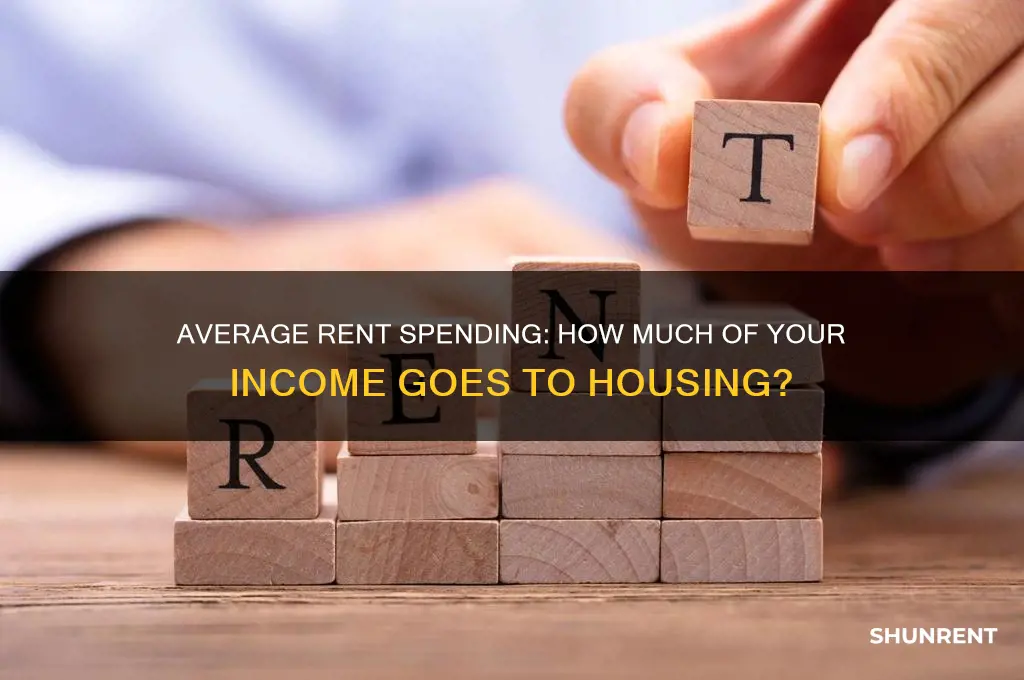

Understanding what percentage of income the average person spends on rent is a critical aspect of financial planning and housing affordability. This metric varies widely depending on geographic location, income levels, and local housing markets. In many urban areas, particularly in high-cost cities like New York or San Francisco, individuals may allocate 30% to 50% or more of their income to rent, often exceeding the recommended 30% threshold advised by financial experts. Conversely, in more affordable regions, this percentage can drop to 20% or less. Factors such as minimum wage laws, cost of living, and government housing policies also play a significant role in shaping these figures. Analyzing this data provides insights into economic disparities, housing accessibility, and the overall financial well-being of individuals across different regions.

| Characteristics | Values |

|---|---|

| Average Rent-to-Income Ratio (U.S.) | 28-30% (varies by source, commonly cited as the 30% rule) |

| Median Rent Burden (U.S.) | ~30% of gross income (National Median Rent, 2023 data) |

| Affordable Housing Threshold | ≤30% of income (HUD definition) |

| Cost-Burdened Households (U.S.) | ~46% of renters spend >30% of income on rent (2022 data) |

| Severely Cost-Burdened Households | ~23% of renters spend >50% of income on rent (2022 data) |

| Global Average (OECD Countries) | ~25-30% (varies by country; e.g., Germany ~25%, U.S. ~30%) |

| High-Cost Cities (e.g., NYC, SF) | 40-50% of income spent on rent (due to housing market pressures) |

| Low-Income Households | Often spend >50% of income on rent (due to affordability challenges) |

| Recommended Budget Rule | 30% of gross income for rent (widely accepted financial guideline) |

| Source Variability | Data ranges based on region, income level, and data collection method |

Explore related products

What You'll Learn

- Regional Rent Variations: Rent percentages differ significantly across cities, states, and countries

- Income-to-Rent Ratio: Ideal rent should be 30% or less of monthly income

- Housing Affordability Crisis: Rising rents outpace income growth in many areas

- Rent Burden by Demographic: Younger and lower-income households spend higher percentages on rent

- Rent vs. Owning a Home: Renting often consumes a larger income percentage than mortgage payments

![]()

Regional Rent Variations: Rent percentages differ significantly across cities, states, and countries

Rent burdens vary wildly depending on where you live. In San Francisco, residents shell out an average of 45% of their income on rent, while in Detroit, that figure drops to around 25%. This stark contrast highlights how regional factors like job markets, housing supply, and local policies create vastly different affordability landscapes. For instance, tech hubs with booming economies often see rents soar as demand outpaces construction, forcing residents to allocate a larger share of their earnings to housing.

Consider the global perspective: In Berlin, rent control policies have historically kept housing costs manageable, with residents spending roughly 20-25% of their income on rent. Contrast this with Hong Kong, where space is at a premium and residents often spend over 60% of their income on housing. These examples underscore the role of government intervention and geographic constraints in shaping rent burdens. Travelers or expats should research local housing markets thoroughly, as what’s considered "affordable" in one city might be unattainable in another.

To navigate these variations, start by benchmarking your rent-to-income ratio against local averages. Financial advisors often recommend keeping housing costs below 30% of your income, but this rule of thumb may be unrealistic in high-cost areas. Instead, prioritize cities or neighborhoods where your desired lifestyle aligns with regional rent realities. For example, if you’re a remote worker, consider relocating to a lower-cost area where your income stretches further. Conversely, if you’re tied to a specific city, explore cost-saving strategies like roommates or rent-stabilized units.

Regional rent disparities also impact long-term financial planning. In cities where rent consumes 40% or more of income, saving for emergencies, retirement, or homeownership becomes significantly harder. To counteract this, residents in high-rent areas should focus on maximizing income through career advancement or side hustles, while also negotiating rent increases or seeking government housing assistance where available. Understanding these regional nuances isn’t just about budgeting—it’s about making informed decisions that align with your financial goals and quality of life.

Understanding Rent-to-Own: Average APR Rates Explained for Buyers

You may want to see also

Explore related products

![]()

Income-to-Rent Ratio: Ideal rent should be 30% or less of monthly income

The 30% rule, a widely accepted guideline in personal finance, suggests that individuals should allocate no more than 30% of their monthly income to rent. This principle, rooted in the Income-to-Rent Ratio, serves as a benchmark for financial stability and affordability. For instance, if your monthly income is $4,000, your rent should ideally not exceed $1,200. This rule is not arbitrary; it stems from historical housing affordability studies and has been adopted by financial advisors and government agencies alike. By adhering to this ratio, individuals can ensure they have sufficient funds for other essential expenses, savings, and discretionary spending.

Analyzing the practicality of the 30% rule reveals its adaptability across different income levels and geographic locations. In high-cost urban areas like New York or San Francisco, where rent prices are exorbitant, sticking to this guideline can be challenging. For example, a median rent of $3,500 in Manhattan would require a monthly income of at least $11,667 to meet the 30% threshold—a figure far above the national median income. Conversely, in more affordable regions, such as the Midwest, adhering to this rule is more feasible. This disparity highlights the need for flexibility in applying the 30% rule, considering local economic conditions and individual circumstances.

To implement the 30% rule effectively, start by calculating your monthly income after taxes. Next, multiply this figure by 0.30 to determine your maximum affordable rent. For example, if your net monthly income is $3,500, your rent should not surpass $1,050. Practical tips include negotiating rent with landlords, considering roommates to split costs, or exploring government housing assistance programs. Additionally, if you’re in a high-rent area, weigh the benefits of living farther from city centers or in smaller spaces to align with this budget.

A comparative analysis of the 30% rule versus other budgeting methods underscores its simplicity and effectiveness. Unlike detailed budgeting systems like the 50/30/20 rule (50% needs, 30% wants, 20% savings), the 30% rule focuses solely on housing, making it easier to apply. However, it may not account for other significant expenses, such as childcare or medical costs. For households with multiple financial obligations, combining this rule with a comprehensive budget ensures a more holistic approach to financial management.

In conclusion, the Income-to-Rent Ratio of 30% or less is a valuable tool for maintaining financial health, but it requires thoughtful application. By understanding its origins, limitations, and practical implementation strategies, individuals can make informed decisions about their housing expenses. Whether you’re a young professional in a bustling city or a family in a suburban area, tailoring this guideline to your unique situation ensures that rent remains a manageable part of your budget, paving the way for long-term financial stability.

Renting an Uber Driver for 8 Hours: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Housing Affordability Crisis: Rising rents outpace income growth in many areas

A staggering 30% of their income is what the average American spends on rent, according to the U.S. Department of Housing and Urban Development. This threshold, once considered the upper limit of affordability, is now the norm for many. However, in cities like San Francisco, Los Angeles, and New York, renters often allocate closer to 50% or more of their earnings to housing. This disparity between rent and income growth is not just a statistic—it’s a crisis reshaping lives and communities.

Consider the mechanics of this imbalance. Since 2010, median rents in the U.S. have risen by 25%, while wages have only increased by 15%. In metropolitan areas, the gap is even starker. For instance, in Miami, rents surged by 40% over the past five years, while incomes grew a mere 10%. This mismatch forces households to cut back on essentials like healthcare, education, and savings. A family earning $50,000 annually, spending 50% on rent, is left with just $2,083 per month for all other expenses—a precarious financial tightrope.

The consequences are systemic. Rent burdens disproportionately affect low-income households, minorities, and young adults. For example, 47% of Black renters and 43% of Hispanic renters are cost-burdened, compared to 38% of white renters. Millennials, often dubbed the "rent-burdened generation," delay homeownership, marriage, and even parenthood due to housing instability. This isn't just an individual struggle—it’s a societal brake on economic mobility and generational wealth-building.

To address this crisis, policymakers must act on multiple fronts. First, expand affordable housing initiatives, such as tax incentives for developers and increased funding for public housing. Second, implement rent control measures, but cautiously—poorly designed policies can reduce housing supply. Third, raise minimum wages and strengthen tenant protections to balance the scales. For individuals, practical steps include negotiating lease terms, exploring roommate arrangements, or relocating to less expensive areas. While no single solution exists, a combination of systemic reforms and personal strategies can mitigate the impact of this growing crisis.

Jonathan Larson's Tragic Death: The Story Behind Rent's Creator

You may want to see also

Explore related products

![]()

Rent Burden by Demographic: Younger and lower-income households spend higher percentages on rent

The average person spends about 30% of their income on rent, but this figure masks significant disparities across demographics. Younger households, particularly those aged 25–34, often allocate closer to 40–45% of their earnings to housing, according to data from the U.S. Census Bureau. This disparity is even more pronounced for lower-income households, where rent can consume upwards of 50% of monthly income, pushing them into what experts call "rent burden"—defined as spending over 30% of income on housing. These groups face a double bind: limited earnings coupled with rising rental costs, leaving little room for savings, emergencies, or upward mobility.

Consider the math for a 28-year-old earning $40,000 annually. If they spend 45% on rent, that’s $1,500 monthly, leaving $1,166 for all other expenses. Now compare this to a 45-year-old earning $70,000, who spends 30% on rent ($1,750 monthly) but has $2,083 left for other needs. The younger earner not only has less disposable income but also faces higher relative housing costs, exacerbating financial strain. This imbalance is further compounded by student loan debt, which disproportionately affects younger demographics, siphoning away funds that could otherwise offset rent burden.

Lower-income households, often defined as those earning below $30,000 annually, are hit hardest. For them, rent burden isn’t just a statistic—it’s a daily reality. A family earning $25,000 might spend $900 monthly on rent, equating to 43% of their income. This leaves a mere $775 for food, transportation, healthcare, and other essentials. Such tight budgets force trade-offs: skipping medical appointments, relying on food assistance, or accumulating debt. Over time, these compromises erode financial stability and limit opportunities for education, career advancement, or homeownership.

To mitigate rent burden, younger and lower-income households can adopt practical strategies. First, consider shared housing or roommate arrangements, which can reduce individual rent costs by 30–50%. Second, explore government assistance programs like Section 8 vouchers or local rent subsidies, which cap housing expenses at 30% of income. Third, negotiate lease terms with landlords, such as offering to sign a longer lease in exchange for a lower monthly rate. Finally, prioritize budgeting tools like the 50/30/20 rule (50% on needs, 30% on wants, 20% on savings), adjusting the "needs" category to account for higher rent while still carving out savings.

The takeaway is clear: rent burden isn’t evenly distributed—it disproportionately affects younger and lower-income households, creating cycles of financial instability. While systemic solutions like affordable housing initiatives are critical, individuals can take proactive steps to ease the strain. By understanding the unique challenges of these demographics and adopting targeted strategies, households can regain control over their finances and build a more secure future.

IDP Requirements for Moped Rentals: What You Need to Know

You may want to see also

Explore related products

$19.99

![]()

Rent vs. Owning a Home: Renting often consumes a larger income percentage than mortgage payments

Rent typically consumes 30% to 50% of a tenant’s monthly income, a figure that far exceeds the 25% to 28% financial advisors recommend for housing. This disparity becomes starker when compared to homeowners with mortgages, who often allocate a smaller percentage of their income to housing after the initial down payment. For instance, a renter earning $4,000 monthly might spend $1,500 on rent, while a homeowner with a similar income could pay $1,000 toward a mortgage, leaving more disposable income for savings, investments, or emergencies. This gap widens in high-cost urban areas, where rent-to-income ratios can soar above 50%, trapping renters in a cycle of financial strain.

Consider the long-term financial implications: renting offers flexibility but lacks equity-building potential. Every rent payment enriches the landlord, not the tenant. In contrast, mortgage payments gradually build home equity, a tangible asset that can appreciate over time. For example, a $200,000 home with a 20% down payment and a 30-year mortgage at 4% interest results in monthly payments of roughly $955. Over 30 years, the homeowner builds $200,000 in equity (excluding appreciation), while the renter has nothing to show for decades of payments. This wealth gap underscores why renting often feels like a financial treadmill.

However, owning isn’t always the better choice. First-time buyers must account for closing costs (2% to 5% of the home price), maintenance (1% to 4% of the home’s value annually), and property taxes. For a $250,000 home, these expenses could add $2,500 to $10,000 yearly, depending on location. Renters avoid these costs but miss out on tax deductions for mortgage interest and property taxes. To decide, calculate your break-even point: compare the total cost of renting (rent + opportunity cost of not investing) to the total cost of owning (mortgage + maintenance + taxes) over 5 to 10 years. If owning costs less and aligns with your long-term goals, it may be the wiser choice.

A practical tip for renters: negotiate rent or seek rent-controlled units to lower your housing burden. For instance, offering to sign a longer lease or pay several months upfront might reduce monthly rent by 5% to 10%. Homebuyers should aim for a 20% down payment to avoid private mortgage insurance (PMI), which adds 0.5% to 1% to monthly payments. Additionally, consider refinancing if interest rates drop significantly—a 1% reduction on a $200,000 mortgage saves roughly $120 monthly. Both renters and buyers should prioritize building an emergency fund to cover 3 to 6 months of living expenses, ensuring financial stability regardless of housing choice.

Ultimately, the rent-vs.-own decision hinges on lifestyle, financial health, and market conditions. Renting suits those prioritizing mobility or unable to afford a down payment, while owning benefits those seeking stability and long-term wealth accumulation. A 25-year-old renting for $1,200 monthly could instead save $600 monthly toward a down payment, reaching 20% on a $200,000 home in 13 years (assuming 3% annual savings growth). Conversely, a 40-year-old with stable income might prioritize owning to secure retirement equity. Tailor your choice to your age, income, and goals, recognizing that renting’s higher income percentage often reflects a trade-off between flexibility and financial growth.

Rents Received vs. Reported Revenues: Understanding Key Financial Differences

You may want to see also

Frequently asked questions

On average, people spend about 30% of their income on rent, though this can vary based on location, income level, and personal circumstances.

Yes, the 30% rule is a common guideline for affordability, but it may not apply to everyone, especially in high-cost areas where rent can exceed this threshold.

In expensive cities like New York or San Francisco, people often spend 40-50% or more of their income on rent, while in more affordable areas, it may be closer to 20-25%.

Spending more than 30% on rent can lead to financial strain, leaving less money for savings, emergencies, and other essential expenses.

Options include finding a roommate, moving to a less expensive area, negotiating rent, or increasing income to better align with housing costs.