The percentage of income allocated to rent varies significantly depending on geographic location, income level, and housing market conditions. In many urban areas, particularly in high-cost cities like New York, San Francisco, or London, renters often spend 30% to 50% or more of their monthly income on housing, far exceeding the commonly recommended 30% threshold. Conversely, in more affordable regions, this figure may drop to 20% or less. Factors such as minimum wage levels, local economies, and government housing policies also play a critical role in determining how much of one’s income goes toward rent. Understanding this percentage is essential for assessing affordability, financial stability, and the broader impact of housing costs on individuals and communities.

| Characteristics | Values |

|---|---|

| Average Rent-to-Income Ratio (U.S.) | 28% (as of 2023, varies by source) |

| Recommended Rent-to-Income Ratio | 30% or less (commonly advised by financial experts) |

| Low-Income Households (U.S.) | Often spend 50% or more of income on rent |

| High-Cost Cities (e.g., NYC, SF) | Up to 40-50% of income spent on rent |

| Global Average (OECD Countries) | ~25-30% of income allocated to housing |

| Minimum Wage Workers (U.S.) | Up to 60-70% of income spent on rent in high-cost areas |

| Median Rent Burden (U.S.) | 24% of income (as of 2023, National Low Income Housing Coalition) |

| Rent Burden Threshold | Households spending >30% of income on rent are considered "rent-burdened" |

| European Average | ~20-25% of income spent on rent |

| Affordable Housing Definition | Housing costing ≤30% of household income |

| Rent Increases (2020-2023) | Average rent increased by 15-20%, outpacing income growth in many areas |

| Source of Data | U.S. Census Bureau, OECD, National Low Income Housing Coalition, etc. |

Explore related products

What You'll Learn

- Median Rent-to-Income Ratios: National and regional averages of rent as a percentage of income

- Affordable Housing Thresholds: Definitions of what constitutes affordable rent (e.g., 30% of income)

- Urban vs. Rural Differences: Rent-to-income disparities between cities and rural areas

- Income Bracket Variations: How rent percentages differ across low, middle, and high-income groups

- Global Rent Burdens: Comparisons of rent-to-income ratios across different countries

![]()

Median Rent-to-Income Ratios: National and regional averages of rent as a percentage of income

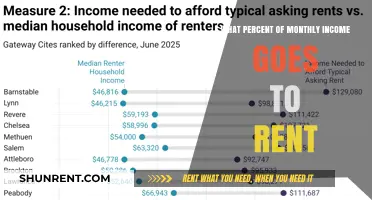

A commonly cited rule of thumb suggests that households should allocate no more than 30% of their income to rent, a benchmark established by the U.S. Department of Housing and Urban Development (HUD). However, median rent-to-income ratios reveal a starkly different reality, particularly when examining national and regional averages. In the United States, the median rent-to-income ratio hovers around 28%, but this figure masks significant disparities. Coastal cities like San Francisco and New York push this ratio above 40%, while more affordable regions in the Midwest and South often fall below 25%. These variations underscore the importance of context when evaluating affordability.

To illustrate, consider Miami, where the median rent consumes 45% of income, compared to Pittsburgh, where it accounts for just 22%. Such differences are not merely statistical—they reflect broader economic and housing market dynamics. High-demand urban centers often experience a mismatch between wage growth and rent increases, leaving residents disproportionately burdened. Conversely, regions with slower population growth and lower housing demand tend to offer more balanced ratios. Understanding these regional nuances is critical for policymakers, renters, and investors alike.

Analyzing these ratios also highlights the challenges faced by low-income households. For instance, in Los Angeles, the median rent-to-income ratio for households earning below $30,000 annually exceeds 60%, far surpassing the 30% affordability threshold. This disparity raises questions about housing equity and the efficacy of current affordability measures. It suggests that a one-size-fits-all approach to rent-to-income ratios may be inadequate, necessitating localized solutions tailored to specific demographic and economic conditions.

For individuals navigating rental markets, these ratios serve as a practical tool for budgeting and decision-making. A simple calculation—dividing monthly rent by pre-tax income—can provide insight into financial sustainability. For example, if your monthly rent is $1,500 and your pre-tax income is $5,000, your rent-to-income ratio is 30%, aligning with the HUD guideline. However, if this ratio exceeds 40%, it may be prudent to explore more affordable housing options or consider relocating to a region with a lower cost of living.

In conclusion, median rent-to-income ratios offer a nuanced perspective on housing affordability, revealing both national trends and regional disparities. By examining these figures, stakeholders can better understand the complexities of rental markets and make informed decisions. Whether you’re a renter, policymaker, or investor, recognizing the variability in these ratios is essential for addressing the pressing issue of housing affordability in a meaningful way.

Efficient Rent Collection: Strategies for Landlords to Secure Tenant Payments

You may want to see also

Explore related products

![]()

Affordable Housing Thresholds: Definitions of what constitutes affordable rent (e.g., 30% of income)

The 30% rule, a widely accepted benchmark, suggests that households should allocate no more than 30% of their gross income to housing costs, including rent and utilities. This guideline, established by the U.S. Department of Housing and Urban Development (HUD) in the 1960s, aims to ensure that individuals and families have sufficient income for other necessities like food, healthcare, and transportation. For example, a household earning $4,000 per month should ideally spend no more than $1,200 on rent. However, this threshold often falls short in high-cost urban areas, where rents can consume 50% or more of income, pushing many into financial strain.

While the 30% rule is a useful starting point, it fails to account for variations in household expenses and income levels. For instance, low-income families may struggle even within this threshold, as they often face higher relative costs for essentials like childcare or medical care. In contrast, higher-income households might comfortably exceed 30% without compromising their financial stability. A more nuanced approach, such as the *residual income method*, considers the remaining income after all essential expenses, providing a clearer picture of affordability. This method is particularly valuable for policymakers designing targeted housing assistance programs.

Critics argue that the 30% rule is outdated, given rising housing costs and stagnant wages. In cities like San Francisco or New York, where median rents exceed $3,000, adhering to this threshold would require incomes of $120,000 or more—far beyond the reach of many residents. Alternative thresholds, such as 40% or even 50%, have been proposed for high-cost regions, though these still risk normalizing unaffordable housing. A more dynamic approach, tied to local median incomes and rents, could offer a realistic definition of affordability, ensuring that thresholds reflect regional economic realities.

Practical tips for renters navigating affordability include prioritizing location based on income, considering shared housing or smaller units, and leveraging rental assistance programs. For instance, in cities with inclusionary zoning policies, some developments offer units at reduced rents for qualifying households. Additionally, renters should factor in utilities, transportation, and other location-specific costs when assessing affordability. While the 30% rule remains a valuable guideline, renters must adapt it to their unique financial circumstances and local market conditions to avoid overextending themselves.

Ultimately, defining affordable rent requires moving beyond one-size-fits-all metrics. Policymakers, developers, and renters must collaborate to create solutions that address the root causes of housing unaffordability, such as supply shortages and income inequality. Until then, individuals can use tools like HUD’s affordability calculators and local housing resources to make informed decisions. By combining broad guidelines with personalized strategies, households can better navigate the complex landscape of affordable housing.

Re-Renting Books on Amazon: A Step-by-Step Guide to Save Money

You may want to see also

Explore related products

![]()

Urban vs. Rural Differences: Rent-to-income disparities between cities and rural areas

The rent-to-income ratio in urban areas often hovers around 30%, a threshold widely considered manageable. In cities like New York or San Francisco, however, this figure can skyrocket to 50% or more, forcing residents to allocate a staggering portion of their earnings to housing. This disparity is driven by high demand for limited space, where professionals and families alike are squeezed by soaring property values. In contrast, rural areas typically see rent-to-income ratios closer to 20%, reflecting lower housing costs and less competition. This stark difference highlights how geography dictates financial strain, with urban dwellers often sacrificing savings, investments, or leisure to keep a roof over their heads.

Consider a hypothetical scenario: a teacher earning $50,000 annually. In a rural town, they might pay $600 monthly in rent, or 14% of their income. In a major city, that same teacher could face $1,500 or more, consuming 36% of their earnings. This example underscores the trade-offs urban residents must make, often prioritizing location over financial flexibility. Rural living, while offering affordability, may limit career opportunities or cultural amenities, creating a lifestyle choice as much as an economic one.

To navigate these disparities, individuals should assess their priorities. For those tied to urban centers, strategies like roommate arrangements, rent-controlled units, or suburban commuting can mitigate costs. Rural dwellers, meanwhile, might leverage lower housing expenses to build savings or invest in remote work capabilities. Policymakers could address this divide by incentivizing affordable urban housing or improving rural infrastructure to attract jobs. Ultimately, understanding these differences empowers individuals to make informed decisions about where—and how—they live.

A cautionary note: while rural living may seem financially appealing, hidden costs like transportation or limited services can offset savings. Urban residents, despite higher rents, often benefit from denser job markets and public transit, reducing car dependency. The key is to calculate total living expenses, not just rent, when comparing locations. For instance, a rural resident spending $400 monthly on commuting could effectively negate their housing savings. Balancing affordability with accessibility remains the challenge in both settings.

In conclusion, the urban-rural rent divide is more than a numbers game—it’s a reflection of lifestyle, opportunity, and compromise. Urban areas demand a premium for proximity to jobs and culture, while rural regions offer affordability at the cost of convenience. By analyzing these trade-offs and adopting practical strategies, individuals can align their housing choices with their long-term goals, whether in the heart of the city or the quiet of the countryside.

Rent Like a Champion Post-Shark Tank: Success or Struggle?

You may want to see also

Explore related products

![]()

Income Bracket Variations: How rent percentages differ across low, middle, and high-income groups

The percentage of income allocated to rent varies dramatically across income brackets, revealing stark disparities in financial flexibility and housing affordability. For low-income households, rent often consumes 30% to 50% or more of their monthly earnings, a burden exacerbated by stagnant wages and rising housing costs. This leaves little room for savings, emergencies, or upward mobility. Middle-income earners fare slightly better, typically spending 20% to 30% of their income on rent, but even this can strain budgets in high-cost urban areas. In contrast, high-income individuals allocate a much smaller share, often 10% to 20%, allowing them to invest in assets, leisure, or additional properties. This divergence underscores how rent disproportionately affects financial stability across income groups.

Consider the practical implications of these percentages. A low-income family earning $30,000 annually might spend $9,000 to $15,000 on rent, leaving minimal funds for healthcare, education, or debt repayment. Meanwhile, a high-income household earning $200,000 could allocate $20,000 to $40,000 to rent while still maintaining a robust savings rate. This disparity isn’t just about numbers—it’s about opportunities. High rent burdens for low-income groups often trap them in cycles of poverty, while those with higher incomes can leverage their remaining funds to build wealth. Policymakers and urban planners must address this imbalance through initiatives like rent control, affordable housing projects, or income-based subsidies.

To illustrate further, let’s compare three hypothetical households. A single parent earning $25,000 annually might pay $1,000 monthly in rent, equating to 48% of their income. A dual-income couple earning $80,000 might spend $1,500 monthly, or 23% of their combined income. A tech executive earning $300,000 could allocate $3,000 monthly, just 12% of their earnings. These scenarios highlight how rent percentages reflect not only income levels but also geographic location, family size, and career stability. For instance, a middle-income family in San Francisco might face rent burdens closer to those of low-income households elsewhere, emphasizing the need for localized solutions.

Persuasively, it’s clear that reducing rent burdens for low- and middle-income groups isn’t just an economic issue—it’s a moral imperative. High rent-to-income ratios stifle social mobility, increase homelessness, and widen wealth gaps. Governments and private sectors must collaborate to create mixed-income housing developments, expand tax incentives for affordable housing, and enforce fair rental practices. Individuals can also take proactive steps, such as negotiating rent terms, exploring roommate arrangements, or relocating to more affordable areas. By addressing these disparities, we can foster more equitable communities where housing doesn’t come at the expense of financial security.

In conclusion, understanding how rent percentages differ across income brackets is crucial for crafting effective solutions. Low-income households face crippling rent burdens, middle-income earners navigate tight budgets, and high-income individuals enjoy financial flexibility. These variations demand targeted interventions, from policy reforms to personal strategies. By prioritizing affordable housing and equitable rent practices, we can ensure that everyone, regardless of income, has access to stable, dignified living conditions.

Calculating Quota Rent Per Pound: A Step-by-Step Guide for Beginners

You may want to see also

Explore related products

![]()

Global Rent Burdens: Comparisons of rent-to-income ratios across different countries

The rent-to-income ratio, a critical metric for assessing housing affordability, varies dramatically across the globe, reflecting disparities in economic conditions, housing policies, and urban development. In New York City, for instance, renters often allocate 40–50% of their income to housing, far exceeding the 30% threshold widely considered manageable. This contrasts sharply with Berlin, where rent control policies have historically kept the ratio closer to 20–25%, though recent market pressures are pushing this upward. Such variations underscore the need for a nuanced understanding of how global cities balance housing demand with affordability.

Analyzing these ratios reveals systemic challenges. In Hong Kong, the world’s least affordable housing market, residents spend upwards of 70% of their income on rent, a consequence of limited land supply and speculative investment. Conversely, in Singapore, government intervention through public housing programs has kept the ratio at around 20–25%, demonstrating the impact of policy on affordability. These examples highlight how geographic, economic, and political factors intersect to shape rent burdens, offering lessons for cities grappling with similar issues.

A comparative approach further illuminates these disparities. In Mumbai, rapid urbanization has driven rent-to-income ratios to 40–50%, as low-income households compete for scarce housing. Meanwhile, in Tokyo, efficient public transit and dense housing development have kept the ratio at 30–35%, despite high living costs. Such comparisons suggest that while income levels play a role, urban planning and policy interventions are equally critical in determining affordability.

For individuals and policymakers, understanding these global trends is essential for addressing rent burdens. Practical steps include advocating for rent control measures, investing in public housing, and promoting mixed-income developments. For renters, budgeting tools and financial literacy programs can help manage high housing costs. Ultimately, the global rent-to-income landscape serves as both a warning and a roadmap: without proactive measures, housing affordability will remain a pressing crisis, but with strategic interventions, it can be mitigated.

Renting vs. Owning: Understanding the Rise of Subscription Services

You may want to see also

Frequently asked questions

On average, people spend about 30% of their income on rent, though this can vary based on location, income level, and personal circumstances.

Yes, spending 50% of income on rent is generally considered excessive and may lead to financial strain. Experts recommend keeping housing costs below 30% of income.

In high-cost cities like New York or San Francisco, people often spend 40-50% or more of their income on rent, while in more affordable areas, it may be closer to 20-25%.

Consider downsizing, finding a roommate, moving to a more affordable area, or increasing your income to reduce the percentage of your income going toward rent.