When determining what you should rent for on an annual income of $55,500, it’s essential to follow the general rule of thumb that housing costs should not exceed 30% of your gross monthly income. For someone earning $55,500, this translates to approximately $1,387 per month for rent. Factors such as location, lifestyle, and financial goals should also be considered. In high-cost-of-living areas, you may need to adjust your budget or consider roommates, while in more affordable regions, you might have room for additional amenities. Prioritizing savings, debt repayment, and other expenses will help ensure your rent remains manageable and aligns with your overall financial health.

Explore related products

What You'll Learn

- Budgeting Basics: Allocate 30% of income for rent, ensuring financial stability and covering other expenses

- Location Priorities: Balance rent costs with proximity to work, amenities, and desired neighborhoods

- Housing Types: Compare apartments, condos, or houses to find the best value for your budget

- Additional Costs: Factor in utilities, parking, and maintenance fees when calculating total housing expenses

- Roommate Options: Sharing space can significantly reduce rent, freeing up funds for savings or leisure

![]()

Budgeting Basics: Allocate 30% of income for rent, ensuring financial stability and covering other expenses

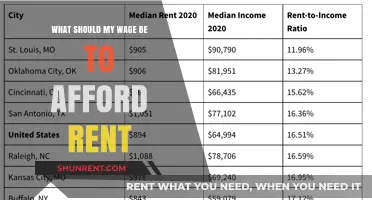

Earning $55,500 annually translates to roughly $4,625 per month before taxes. Following the 30% rule, you should aim to spend no more than $1,387.50 on rent monthly. This benchmark isn’t arbitrary—it’s a widely accepted guideline to prevent housing costs from overwhelming your budget. Exceeding this threshold risks squeezing out funds for essentials like groceries, utilities, and savings. For context, if you’re eyeing a studio in a mid-tier city, this budget might suffice, but in pricier markets, you’ll need to adjust expectations or consider roommates.

Let’s break it down further. If you allocate $1,387.50 to rent, that leaves approximately $3,237.50 for other monthly expenses. This includes $500–$600 for groceries, $200–$300 for utilities, $100–$200 for transportation, and ideally, $500–$800 for savings or debt repayment. See how quickly the numbers add up? Sticking to the 30% rule ensures you’re not just surviving but also building financial resilience. For instance, if your car breaks down or you face an unexpected medical bill, you’re less likely to derail your budget.

Now, consider the trade-offs. Renting a one-bedroom apartment for $1,500 might feel tempting, but it exceeds your 30% limit by $112.50. That small overrun could mean cutting back on retirement contributions or eating out less—or worse, relying on credit cards. Conversely, opting for a $1,200 rental leaves you with an extra $187.50 monthly, which could fund a vacation or boost your emergency fund. The key is to prioritize long-term stability over short-term comfort.

Here’s a practical tip: Use online calculators to factor in local costs of living. For example, in Austin, Texas, $1,387.50 might secure a modest one-bedroom, while in San Francisco, it may only cover a shared space. Adjust your expectations based on location, but don’t compromise the 30% rule. If necessary, look for ways to increase income—like a side hustle—rather than stretching your housing budget.

Finally, remember that rent isn’t the only housing expense. Factor in utilities, internet, and renters’ insurance, which can add $100–$200 monthly. If your rent is already at the 30% limit, these extras could push you over the edge. Negotiate rent, split costs with roommates, or seek properties where utilities are included. By staying disciplined and creative, you can adhere to the 30% rule while still finding a place that feels like home.

Renting Prison Buses and Orange Jumpsuits: Legal or Illegal?

You may want to see also

Explore related products

![]()

Location Priorities: Balance rent costs with proximity to work, amenities, and desired neighborhoods

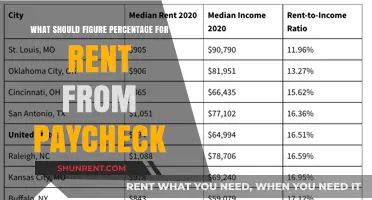

Earning $55,500 annually translates to roughly $4,625 per month before taxes. Financial advisors recommend spending no more than 30% of your income on rent, capping your budget at $1,388 monthly. However, this figure often clashes with the reality of high-demand urban areas, where rents can easily surpass this threshold. To navigate this tension, prioritize location strategically, balancing affordability with access to work, amenities, and desirable neighborhoods.

Consider the trade-offs between living closer to your workplace versus in a more affordable area. For instance, a studio apartment within walking distance to your office might cost $1,600, exceeding your budget but saving you $200 monthly in commuting costs and two hours daily in transit. Conversely, a one-bedroom 20 minutes away could cost $1,200, fitting your budget but adding $100 in monthly transportation expenses and an hour of daily commuting. Calculate the net cost and time savings to determine which option aligns better with your lifestyle priorities.

Amenities play a pivotal role in location decisions, but their value varies by individual. Proximity to gyms, grocery stores, and entertainment can justify higher rent if they enhance your daily life significantly. For example, living in a building with an on-site gym might save you $50 monthly in membership fees, effectively lowering your net rent. Conversely, if you rarely use public transportation, living near a subway station may not warrant a premium. Assess which amenities are non-negotiable and which are nice-to-haves to avoid overpaying for conveniences you won’t utilize.

Desired neighborhoods often come with a price tag, but there are ways to maximize value. Look for up-and-coming areas adjacent to popular neighborhoods, where rents are lower but still offer access to the same amenities. For instance, renting in a neighborhood bordering a trendy district can save you 15-20% on rent while keeping you within walking distance of its attractions. Additionally, consider older buildings or units with fewer frills, which often offer more square footage for the same price as newer, amenity-rich complexes.

Ultimately, location priorities require a personalized approach. Map out your daily routines, work commute, and leisure activities to identify areas that minimize disruptions while staying within budget. Use tools like rent comparison websites and neighborhood guides to explore options systematically. Remember, the "perfect" location doesn’t exist—it’s about finding the right balance between cost, convenience, and community that aligns with your unique needs and financial constraints.

Discovering Truro, MA: Average Rent and Housing Insights

You may want to see also

Explore related products

![]()

Housing Types: Compare apartments, condos, or houses to find the best value for your budget

Earning $55,500 annually places you in a position to explore various housing options, but the key to maximizing your budget lies in understanding the nuances of each housing type. Apartments, condos, and houses each offer distinct advantages and trade-offs, and your choice should align with your lifestyle, financial goals, and long-term plans. Let’s break down the value proposition of each to help you decide.

Apartments: The Low-Maintenance Option

Renting an apartment is often the most straightforward choice for those seeking convenience and minimal responsibility. Monthly rents typically include utilities like water, trash, and sometimes even internet, simplifying budgeting. Apartments also come with amenities such as gyms, pools, or on-site maintenance, which can save you money on external memberships or repairs. For someone earning $55,500, allocating 30% of your income to housing (a common rule of thumb) means aiming for rent around $1,388 monthly. In many markets, this budget can secure a one-bedroom apartment in a decent neighborhood, especially if you’re willing to compromise on square footage or distance from city centers. The trade-off? Limited privacy, potential noise from neighbors, and fewer opportunities to build equity.

Condos: A Middle Ground with Ownership Perks

Condos blur the line between renting and owning, offering more privacy than apartments while still providing shared amenities like security, landscaping, or community spaces. Renting a condo often means dealing directly with an owner, which can lead to more stable lease terms but fewer included utilities. For $55,500 earners, condos might be slightly pricier than apartments, but they often come with better finishes, more space, and a sense of exclusivity. If you’re considering this route, factor in additional costs like HOA fees (if applicable) and utilities. The upside? Condos can feel more like a home without the maintenance demands of a house, making them ideal for those who value comfort but aren’t ready for full homeownership.

Houses: Space and Flexibility at a Cost

Renting a house offers unparalleled space, privacy, and freedom to customize your living environment. For $55,500 earners, this option may require stretching your budget or finding a roommate to share expenses. Houses often come with additional costs like lawn care, snow removal, and higher utility bills due to larger square footage. However, they’re perfect for those needing room for pets, families, or home offices. If you’re willing to live in suburban or rural areas, your budget can go further, potentially securing a 2–3 bedroom home. The key is balancing your desire for space with the ongoing maintenance and utility costs, which can add up quickly.

Comparative Analysis: What’s the Best Value?

To determine the best value, consider your priorities. Apartments offer affordability and convenience, making them ideal for singles or couples prioritizing low overhead. Condos provide a step up in quality and privacy, suitable for those willing to pay a premium for a more polished living experience. Houses deliver space and independence but require a larger financial commitment and time investment for upkeep. For a $55,500 income, apartments often provide the most bang for your buck, while condos and houses may require trade-offs in location or additional expenses.

Practical Tips for Decision-Making

Start by listing your non-negotiables (e.g., pet-friendly, parking, laundry) and nice-to-haves (e.g., gym, balcony). Use rental platforms to compare prices in your desired areas, and don’t forget to factor in hidden costs like parking fees or pet rent. If you’re leaning toward a house, consider the long-term commitment and whether you’re prepared for unexpected repairs. Ultimately, the best value is the option that aligns with your lifestyle and financial goals without straining your budget.

Mastering Prepaid Rent Accounting: Balance Sheet Entry Guide

You may want to see also

Explore related products

$9.91 $26.99

![]()

Additional Costs: Factor in utilities, parking, and maintenance fees when calculating total housing expenses

Renting a home on a $55,500 salary requires a meticulous approach to budgeting, and one critical aspect often overlooked is the additional costs that accompany your monthly rent. These hidden expenses can significantly impact your financial stability if not accounted for. Let's delve into the specifics of utilities, parking, and maintenance fees, ensuring you make an informed decision.

Utilities: The Variable Expense

When considering utilities, it's essential to understand that costs can fluctuate. On average, a single person might spend around $100 to $200 monthly on utilities, including electricity, water, and gas. However, this range can vary based on factors like climate, apartment size, and personal usage habits. For instance, a studio apartment in a mild climate may result in lower heating and cooling costs compared to a larger space in an extreme weather region. To manage this variable, consider researching average utility costs in your desired neighborhood and adopting energy-efficient practices to keep expenses predictable.

Parking: A Necessary Evil or Optional Extra?

Parking fees can be a significant addition to your housing expenses, especially in urban areas. In some cities, monthly parking rates can range from $150 to $300 or more, depending on the location and type of parking (garage, lot, or street). If you own a car, this is a crucial consideration. Alternatively, evaluate the feasibility of public transportation or ride-sharing services, which could potentially save you hundreds of dollars each month. For those with vehicles, consider the proximity of parking to your residence and the associated costs, as these can impact your daily routine and overall budget.

Maintenance Fees: Unexpected Surprises

Maintenance and repair costs are often overlooked but can be substantial. While some rentals include maintenance in the rent, others may require tenants to handle these expenses. On average, setting aside $50 to $100 per month for maintenance can be a prudent decision. This fund can cover minor repairs, appliance replacements, or unexpected issues like plumbing emergencies. By planning for these costs, you avoid financial strain when unforeseen maintenance needs arise.

In the context of a $55,500 income, these additional costs can make a substantial difference in your overall housing affordability. A comprehensive approach to budgeting should include these expenses, ensuring you don't overextend your finances. By understanding and preparing for utilities, parking, and maintenance fees, you can make a well-informed decision about the rent you can comfortably afford, creating a stable and stress-free living environment. This detailed consideration of additional costs is a crucial step in the renting process, offering a realistic perspective on your financial capabilities.

Buyer Beware: Understanding Caveat Emptor in Storage Unit Rentals

You may want to see also

Explore related products

![]()

Roommate Options: Sharing space can significantly reduce rent, freeing up funds for savings or leisure

Earning $55,500 annually places you in a bracket where rent can easily consume a disproportionate share of your income, especially in high-cost urban areas. The 30% rule suggests allocating no more than $1,387.50 monthly for housing, but in cities like New York or San Francisco, this barely covers a studio. Sharing space with roommates emerges as a strategic solution, slashing rent by 30–50% while maintaining access to desirable neighborhoods. For instance, splitting a $2,200 two-bedroom apartment reduces your share to $1,100, freeing up $287.50 monthly—funds better spent on emergencies, investments, or experiences.

When selecting a roommate, compatibility extends beyond personality. Treat it as a business partnership: draft a written agreement outlining rent division, utility responsibilities, and guest policies. Platforms like SpareRoom or Facebook Groups can connect you with vetted candidates, but always conduct interviews to assess lifestyle alignment. For example, a night owl paired with an early riser may lead to friction, while shared interests in sustainability could foster harmony. Age and profession matter too; a graduate student might prioritize quiet evenings, whereas a freelance designer may thrive in a collaborative environment.

The financial benefits of roommates compound over time. Saving $287.50 monthly translates to $3,450 annually—enough for a vacation, a 401(k) boost, or debt repayment. However, shared living requires boundaries. Invest in noise-canceling headphones, establish communal area schedules, and designate private spaces to preserve sanity. Apps like Splitwise streamline expense tracking, preventing resentment over shared groceries or streaming services. Remember, the goal isn’t merely to cut costs but to enhance your quality of life by allocating resources to what truly matters.

Critics argue that roommates compromise privacy, but strategic planning mitigates this. Opt for apartments with en-suite bathrooms or larger common areas to reduce overlap. If cohabitating long-term, consider a three-bedroom unit where one room doubles as a home office or gym, adding value beyond rent reduction. Alternatively, house-sharing with a live-in landlord can offer stability, though at the cost of autonomy. Weigh these trade-offs against your financial goals: is your priority maximizing savings, or are you willing to spend slightly more for added comfort?

Ultimately, roommates aren’t just a cost-saving measure—they’re a lifestyle choice. For someone earning $55,500, this decision can mean the difference between scraping by and thriving. By treating shared living as a deliberate strategy rather than a last resort, you reclaim control over your budget and time. Whether saving for a down payment or funding a passion project, the extra $3,450 annually becomes a tool for building the life you want, not just the one you can afford.

Renting 'The Spy Who Dumped Me': A Quick Guide to Streaming

You may want to see also

Frequently asked questions

A common rule of thumb is the 30% rule, which suggests spending no more than 30% of your gross income on rent. For $55,500, that would be approximately $1,387.50 per month.

While $1,500 is slightly above the 30% threshold ($1,387.50), it may still be manageable if you have minimal debt and low expenses. However, it’s important to budget carefully to ensure you can cover other necessities and savings.

Sharing rent with roommates can significantly lower your housing costs, allowing you to stay within the 30% rule or save more. It’s a practical option if you’re looking to maximize savings or live in a higher-cost area.

After allocating $1,400 for rent (about 31% of your income), aim to save at least 10-20% of your net income for emergencies, retirement, and other financial goals. Adjust your budget to prioritize savings after covering essentials.

Renting is often more flexible and requires less upfront cost, making it suitable for those with limited savings or uncertain plans. Buying may be an option if you have a stable income, savings for a down payment, and long-term plans to stay in one location. Consult a financial advisor to determine the best choice for your situation.